On June 10, the U.S. Department of the Treasury issued a preview of the forthcoming guidance implementing the Education Freedom Tax Credit (EFTC) scholarship program, which is set to take effect on Jan. 1, 2027. President Donald Trump (R) enacted the tax credit as part of the One Big Beautiful Bill Act (OBBBA). The statute required the Treasury to create regulations to implement the program. Deputy Assistant Secretary for Tax Policy Kevin Salinger said the Treasury would propose regulations in September.

The EFTC is a nonrefundable tax credit, allowing individuals to receive federal tax credits for donations up to $1,700 to authorized scholarship-granting organizations (SGOs). It is a dollar-for-dollar nonrefundable tax credit, meaning individuals can lower their federal tax liability by $1 for every $1 donated to accredited SGOs; if a taxpayer donates more than $1,700, they will not receive a tax refund for the amount over $1,700. The total amount of credits the program can offer is not capped.

SGOs distribute donated scholarship funds to eligible families for a variety of private or public educational expenses, including private school tuition, tutoring services, textbooks, and more. To qualify for scholarships, students had to live in households earning no more than 300% of the area's median gross income (AGMI) and be eligible to enroll in K-12 schools. EdChoice published an interactive U.S. map on May 21, 2026, displaying what 300% of AGMI would be for FY 2026 across the country. The program will take effect January 1, 2027.

States that elect to participate must submit a list of SGOs that taxpayers can donate to in order to receive the federal tax credit. Students in states that do not opt in cannot receive scholarships funded under the program, but donors in those states can still receive a federal tax credit by donating to SGOs in participating states. As enacted, the program will not affect state budgets.

The June 10 preview laid out the intent of the Treasury to issue nine specific policies regarding the tax credit.

The 90-percent spending requirement

The OBBBA requires the SGOs to spend 90% of their income on scholarships. When the Treasury requested comments for implementing the program in November 2025, several commenters said that the requirement may not be realistic for some SGOs. Regarding the regulations the Treasury intends to propose in September, it said: "We expect the proposed rules will generally measure the 90-percent spending requirement against the organization’s total receipts, unreduced by expenses. But if the organization’s activities are largely scholarship-granting activities, the organization could use a safe harbor under which 'income of the organization' is measured by the amount held in a section 25F segregated account, including qualified contributions and earnings. For a multistate SGO, that safe harbor would have to be satisfied separately for each State-specific segregated account."

SGO location

The statute requires SGOs to be located in a state that has opted into the scholarship program. The Treasury clarified that, because multi-state SGOs could participate in the program, the Treasury would define “located in” a state as meaning it is authorized to do business in that state and is compliant with state charitable-organization rules. However, the Treasury said it would prohibit states from imposing more restrictive requirements than those enacted in the OBBBA (see those requirements here).

Multi-state SGOs

The Treasury said the regulations would create a way for SGOs operating in multiple states to participate in the program, probably by requiring them to maintain separate donation accounts for each state.

Eligible schools

The Treasury said that it will define "school" to establish which schools could accept from this program. It said "school" would include public and private schools, as well as homeschools in states that treat them as schools under state law. The preview did not specify whether micro-schools would be included in the definition.

Student income qualification verification

The Treasury said the regulations would ensure SGOs verified students' incomes, probably by allowing SGOs to verify household income through paystubs, tax returns, IRS transcripts, W-2s, crediting agencies, or commercial data sources. It would also allow SGOs to categorically verify eligibility for families receiving federal need-based aid and foster students.

Fraud and abuse

The Treasury said that participating SGOs will need to be audited annually. Smaller SGOs could obtain an audit from an internal committee unrelated to their management, while larger SGOs would need a third-party audit.

Donor reporting

The Treasury said it would require SGOs to provide donors "a timely written acknowledgment of their annual contributions, including the total amount of the donor’s qualified contributions and a unique donor number generated under an IRS-provided method." This aims to prevent SGOs from collecting donors' Social Security numbers.

SGO portal

The Treasury said it was considering creating a portal to make it easier for SGOs and the IRS to interact.

Section 530 eligible expenses

The OBBBA defines eligible expenses as those listed in 26 U.S. Code 530(b)(3)(A). The Treasury said that guidance would be important in clarifying what exactly could count as a qualified expense under that definition. The Treasury said it would issue guidance separate from the forthcoming September guidance regarding eligible expenses.

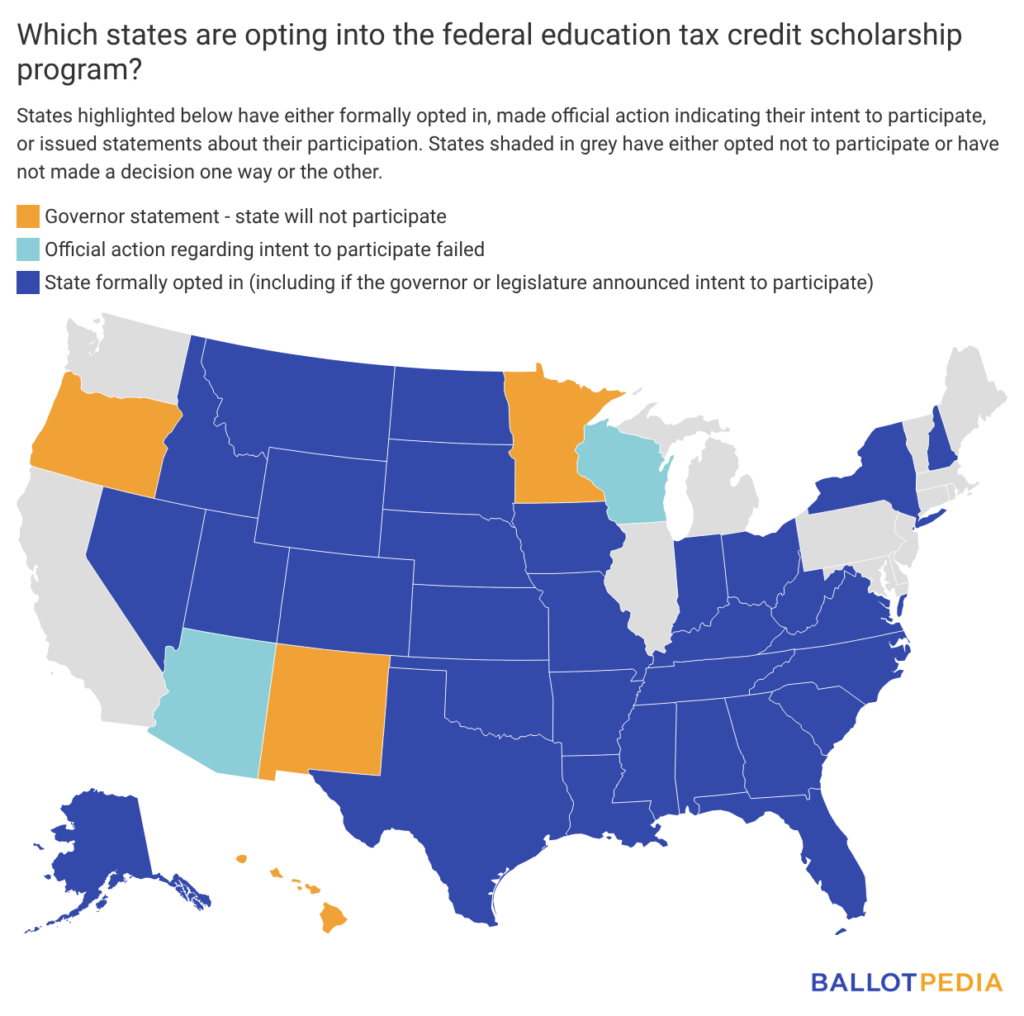

Zooming out

According to EducationWeek, Governors of several Democratic states said they are waiting for the Treasury to issue guidance before deciding whether to participate in the program, even after the June 10 preview. On June 12, Oregon Governor Tina Kotek (D) said that her state would not participate in the program after reviewing it.

As of June 15, 31 states have either opted in to the program or indicated that they plan to.

Partisan breakdown of states that have indicated participation

- Six have Democratic trifectas. Virginia, Colorado, and New York — have said they will participate in the program, while three states — Hawaii, New Mexico, and Oregon — have said they would not participate, though all three governors of those states are reconsidering participation, according to EducationWeek.

- Twenty-three have Republican trifectas. All twenty-three states — Alabama, Arkansas, Florida, Georgia, Idaho, Indiana, Iowa, Louisiana, Mississippi, Missouri, Montana, Nebraska, New Hampshire, North Dakota, Ohio, Oklahoma, South Carolina, South Dakota, Tennessee, Texas, Utah, West Virginia, and Wyoming — said they would participate in the program.

- Eight have divided governments. The Republican-controlled legislatures in Kansas, Kentucky, and North Carolina overrode their Democratic governors' vetoes of bills requiring the state to opt into the program. In Arizona and Wisconsin, legislation to indicate participation failed. Alaska and Nevada formally opted into the program. Minnesota Governor Tim Walz (D) said in March 2026 that the state would not participate in the program.