In this week’s edition of Economy and Society:

- Net Zero Asset Managers relaunches with fewer U.S. firms

- European Council adopts simplified climate reporting rules

- UK adopts voluntary sustainability reporting standards

- Vanguard settles Texas-led antitrust lawsuit for $29.5 million

- California sets August 2026 climate reporting deadline

- ESG legislation update

On Wall Street and in the private sector

Net Zero Asset Managers relaunches with fewer U.S. firms

What’s the story?

On Feb. 25, the Net Zero Asset Managers (NZAM) initiative announced its relaunch with 253 signatories after suspending operations for a year. The coalition revised its membership commitments, removing explicit references to aligning portfolios with a goal of reaching net zero emissions by 2050 and instead allowing firms to set their own climate targets and strategies.

NZAM reported 330 signatories overseeing $57.5 trillion in assets under management as of October 2024. Before the suspension, 44 U.S. firms were members. Following the relaunch, 12 U.S. companies are members, with several large American asset managers remaining absent.

Why does it matter?

The relaunch follows sustained political and legal scrutiny of climate-focused investor coordination in the United States. Republican state attorneys general and federal officials have argued that coordinated climate commitments by large asset managers raise antitrust concerns. NZAM said the revised framework clarifies that participating firms independently set their own climate targets and strategies and use the initiative to disclose how they manage climate-related financial risks and opportunities.

By removing explicit net-zero-by-2050 alignment language and emphasizing that members independently set targets, NZAM appears to be responding to that scrutiny. The limited U.S. participation suggests many American firms remain cautious about joining climate alliances amid ongoing political and legal debate.

What’s the background?

NZAM launched in December 2020 as part of the Glasgow Financial Alliance for Net Zero, which describes itself as “an independent, private-sector-led initiative focused on mobilizing capital and removing barriers to investment in the global transition,” with the goal of aligning financial institutions with reaching net zero greenhouse gas emissions by 2050.

In early 2025, BlackRock exited the initiative, citing legal inquiries from public officials. Soon after, NZAM suspended its activities and began reviewing its commitment framework.

Around the world

European Council adopts simplified climate reporting rules

What’s the story?

The European Council voted to adopt simplified versions of the European Union’s two flagship climate reporting laws — the Corporate Sustainability Reporting Directive (CSRD) and the Corporate Sustainability Due Diligence Directive (CSDDD) — finalizing a reform package that the European Parliament approved in December.

Under the revised rules, the CSRD will apply to companies with more than 1,000 employees and €450 million ($531 million) in annual revenue. The CSDDD will apply to companies with more than 5,000 employees and €1.5 billion ($1.77 billion) in annual revenue. The changes narrow the scope of both laws and adjust compliance timelines. Member states must now incorporate the updated directives into national law.

The adopted package also caps penalties under the CSDDD at 3% of a company’s global net revenue, removes EU-level civil liability, and gives member states additional time to integrate the changes into national regulatory frameworks. Companies that were initially included in the first wave of CSRD reporting but now fall below the revised thresholds will be exempt from compliance under the updated framework.

Why does it matter?

The revised thresholds are expected to remove most previously covered firms from the scope of the laws, significantly reducing the number of companies that must report sustainability data or conduct formal due diligence. The Council also delayed the first wave of CSDDD compliance to 2029 and removed certain obligations, including a requirement for companies to adopt and publish transition plans.

The vote concludes a yearlong debate over whether the EU’s climate disclosure framework imposed disproportionate burdens on businesses. Supporters of the revisions said the changes would reduce administrative costs, while critics said narrowing the scope could weaken transparency and accountability.

What’s the background?

The European Commission proposed amendments to the directives in 2025 as part of a broader effort to simplify EU regulations and improve competitiveness. Legislators previously delayed implementation timelines while negotiating the revisions.

In December, the European Parliament approved a package scaling back reporting requirements and narrowing the number of companies covered, setting the stage for the Council’s final vote.

UK adopts voluntary sustainability reporting standards

What’s the story?

The UK government released finalized UK Sustainability Reporting Standards (UK SRS). The standards are modeled after the International Financial Reporting Standards Foundation’s (IFRS) sustainability and climate disclosure framework. They correspond to the International Sustainability Standards Board’s (ISSB) requirements and are intended to standardize sustainability and climate-related financial disclosures.

For now, the standards are voluntary. However, the Financial Conduct Authority is considering whether to require listed companies to include UK SRS-based disclosures in their reporting. The government also said it will consider whether to require private companies to report under UK SRS as part of a broader review of corporate reporting requirements.

Why does it matter?

The finalized standards align the country’s sustainability reporting framework with the IFRS-based model used or considered in other jurisdictions. The government said the goal is to enable consistent and standardized sustainability and climate-related financial disclosures, while leaving any mandatory application to future regulatory or legislative decisions.

The standards also modify certain transition reliefs. Unlike the IFRS climate standard, which provides a one-year temporary exemption for reporting Scope 3 emissions, the UK version removes a specific time limit for that relief. This means companies may continue relying on the exemption unless regulators later impose a deadline, shifting the decision on when full Scope 3 disclosure is required to future rulemaking rather than embedding it in the standard itself.

What’s the background?

The UK published draft versions of the standards in June 2025 and sought feedback on proposed amendments, including adjustments to transitional reporting reliefs. The Sustainability Disclosure Technical Advisory Committee provided recommendations during the drafting process.

The UK’s move follows developments in other jurisdictions adopting or taking steps to incorporate the IFRS Sustainability Disclosure Standards into their regulatory frameworks. As of mid-2025, 36 jurisdictions had announced plans to use or align with the standards, according to public reporting.

In the states

Vanguard settles Texas-led antitrust lawsuit for $29.5 million

What’s the story?

Vanguard agreed to pay $29.5 million to settle an antitrust lawsuit led by Texas Attorney General Ken Paxton (R), who is running in the March 3, 2026 Republican primary for U.S. Senate, and 10 other Republican-led states. The case, filed in 2024, alleged Vanguard, BlackRock, and State Street used their positions as major shareholders to coordinate pressure on coal companies to reduce output, which the states said resulted in higher electricity costs.

The settlement states Vanguard did not admit wrongdoing and said it agreed to resolve the case to avoid the burden and expense of continued litigation. BlackRock and State Street have not announced settlements and remain defendants.

Why does it matter?

The settlement marks the first resolution in a case testing whether coordinated climate-related shareholder engagement by large index fund managers could violate federal antitrust law.

Because the case continues against BlackRock and State Street, and a federal judge in August 2025 allowed most of the states’ antitrust claims to proceed, courts may still address whether participation in climate investor initiatives and coordinated stewardship efforts amount to unlawful market conduct.

What’s the background?

In November 2024, Texas and 10 other Republican-led states filed the lawsuit in the U.S. District Court for the Eastern District of Texas alleging the asset managers acquired large stakes in major coal producers and used their influence to encourage production cuts aligned with environmental goals.

In May 2025, the U.S. Department of Justice and Federal Trade Commission filed a statement of interest supporting parts of the states’ antitrust claims, saying coordinated ESG-related activity among large asset managers could raise competition concerns.

California sets August 2026 climate reporting deadline

What’s the story?

The California Air Resources Board (CARB) approved final regulations implementing the state’s corporate climate disclosure laws, SB 253 and SB 261, establishing Aug. 10, 2026 as the first reporting deadline for greenhouse gas emissions. The regulations, titled the California Greenhouse Gas Reporting and Climate Financial Risk Disclosure Initial Regulation, outline definitions, compliance fees, and reporting timelines.

Under SB 253, companies with more than $1 billion in annual revenue that do business in California must report Scope 1 and 2 emissions beginning in 2026. Scope 3 emissions — those from a company’s value chain — will be required starting in 2027.

SB 261, which applies to companies with more than $500 million in revenue, requires disclosure of climate-related financial risk. Enforcement of SB 261 is currently paused under a federal appeals court injunction, making compliance voluntary for now.

Why does it matter?

The rules would create one of the most expansive state-level corporate climate disclosure frameworks in the United States. Thousands of companies nationwide could fall under the laws’ reporting requirements because they do business in California.

At the same time, ongoing litigation creates uncertainty. While SB 253 remains in effect, SB 261’s enforcement pause means companies face mixed compliance obligations depending on the outcome of the appeal.

What’s the background?

Gov. Gavin Newsom (D) signed SB 253 and SB 261 into law in October 2023. SB 253 requires annual greenhouse gas emissions reporting, while SB 261 requires biennial disclosure of climate-related financial risks and mitigation strategies. California regulators previously identified more than 4,000 companies that could be subject to the laws.

Business groups challenged both statutes in federal court. The U.S. Court of Appeals for the Ninth Circuit paused enforcement of SB 261 in late 2025 while allowing SB 253 to proceed as litigation continues.

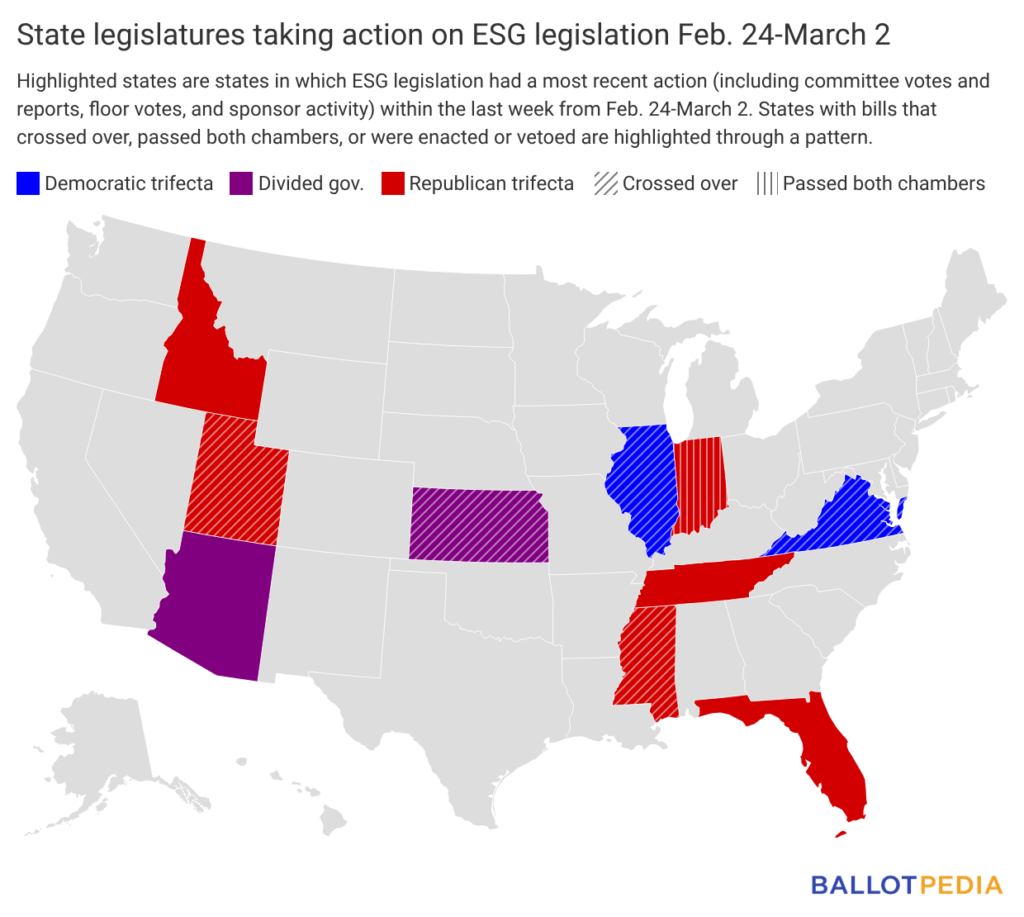

ESG legislation update

Ten states took action on 21 ESG-related bills last week (since Feb 24).

States with legislative activity on ESG last week are highlighted in the map below. Click here to see the details of each bill in the legislation tracker.