In this week’s edition of Economy and Society:

- SEC chairman cites shutdown for shareholder proposal review change

- Study finds EU sustainability reports becoming more standardized

- ESG legislation update

- New partnership aims to improve supply chain emissions reporting

- Activist group disputes BP decision to exclude proposal

- Study finds ESG funds still holding BP shares

In Washington, D.C.

SEC chairman cites shutdown for shareholder proposal review change

What’s the story?

On March 9, 2026, U.S. Securities and Exchange Commission (SEC) Chairman Paul Atkins said that the 2025 federal government shutdown led the SEC to suspend reviews of shareholder proposals due to staffing constraints. Speaking at the Council of Institutional Investors conference in Washington, D.C., Atkins said the SEC suspended most staff reviews of shareholder proposals until after the government reopened following a 42-day shutdown.

The SEC said in November 2025 that it would stop responding to most no-action requests during the 2025–26 proxy season. Atkins explained that SEC staff came back after the shutdown to a large volume of registration statements tied to time-sensitive prospective listings.

Companies excluded a large number of proposals under the new process, and Atkins had not heard broad investor backlash. He also said some filers have sued companies using the process and that the SEC will assess the results after this year’s proxy season.

"You'd be surprised at the amount of work that goes into analyzing these proposals and then rarely do they get majorities, so I think the view internally was mixed at best," Atkins said.

Why does it matter?

The change shifted more responsibility for exclusion decisions from SEC staff to companies. Instead of receiving the agency’s usual no-action responses, companies had to decide for themselves whether proposals could be omitted from proxy materials under SEC rules.

That matters because shareholder proposals often cover environmental and social issues, and investors and companies have traditionally relied on SEC staff views when disputes arise over whether those proposals belong on the ballot.

What’s the background?

The SEC’s Division of Corporation Finance announced in November 2025 that it would continue offering views only on exclusion requests involving a company’s jurisdiction under state law.

Rule 14a-8 allows shareholders to submit proposals for inclusion in company proxy statements. Companies have traditionally sought SEC no-action letters when they want to exclude a proposal, and those letters indicate whether staff would recommend enforcement action.

Around the world

Study finds EU sustainability reports becoming more standardized

What’s the story?

An analysis of more than 1,100 early sustainability reports filed under the European Union’s Corporate Sustainability Reporting Directive (CSRD) finds the rule is making corporate sustainability disclosures longer, more standardized, and less narrative-driven. The review examined more than 1,100 early CSRD reports and suggests the directive is shifting sustainability reporting away from marketing-style publications toward regulatory disclosures similar to financial filings.

Researchers publishing through the Sustainability Reporting Navigator, an open-access academic network, said the directive is changing both the format and tone of sustainability reporting across European companies.

“These kind of sustainability reports are less PR, more 10-K-like,” said Maximilian Müller, a financial accounting researcher at the University of Cologne involved in the analysis, referencing the annual report that public companies must submit.

The study also found companies are relying heavily on major accounting firms to verify sustainability disclosures under the directive’s assurance requirements.

Key findings

Researchers identified several changes in corporate reporting:

- Reports are roughly 30% longer than earlier sustainability disclosures from the same companies.

- Standardized metrics limit company-designed narratives, requiring firms to report comparable environmental and social indicators.

- Verification is concentrated among the Big Four accounting firms—KPMG, PwC, EY, and Deloitte.

- Companies are restating earlier sustainability data as they adopt standardized calculation methods.

Researchers said standardized metrics allow investors to compare companies more directly than under earlier voluntary frameworks.

What’s the background?

The European Union adopted the Corporate Sustainability Reporting Directive in 2022 and implemented it in 2023. It requires companies to disclose standardized environmental and social metrics as part of corporate reporting. The directive remains under political debate.

In December 2026, the European Parliament voted 428–218 to approve legislation scaling back portions of CSRD and related sustainability rules including changes that would exempt many companies from reporting requirements and modify compliance obligations for firms still covered.

In the states

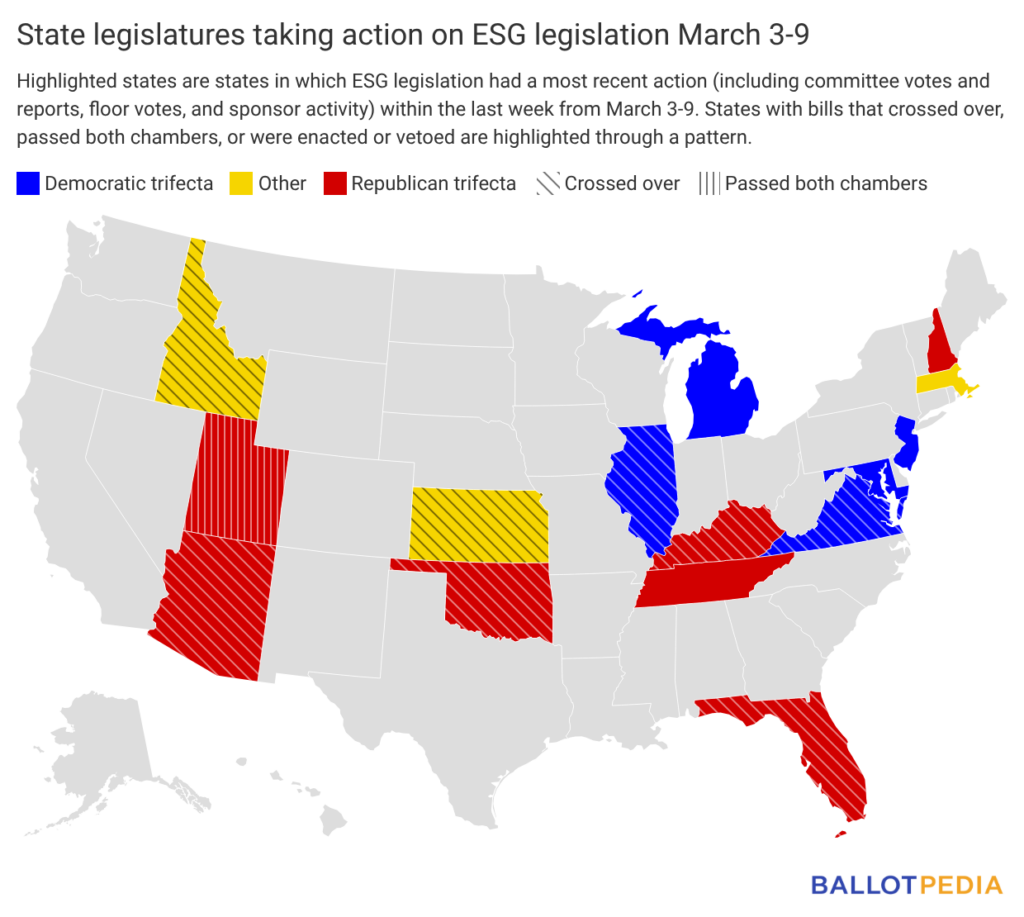

ESG legislation update

Fifteen states took action on 28 ESG-related bills last week (since March 10, 2026).

States with legislative activity on ESG last week are highlighted in the map below. Click here to see the details of each bill in the legislation tracker.

On Wall Street and in the private sector

New partnership aims to improve supply chain emissions reporting

What’s the story?

On March 12, 2026, sustainability ratings firm EcoVadis and climate data company Watershed announced a new partnership last week aimed at improving how companies measure and report Scope 3 emissions, the indirect greenhouse gas emissions produced across corporate supply chains. Scope 3 emissions are the most difficult to measure because they include activity outside a company’s direct operations, such as suppliers, transportation, and product use.

The companies said the partnership will integrate EcoVadis’ supplier emissions data into Watershed’s carbon accounting platform. The goal is to replace industry averages with supplier-specific emissions data so companies can track supply chain emissions and make lower-carbon sourcing decisions.

David Ban, head of data partnerships at Watershed, said: "Unlocking the next generation of Scope 3 emissions reduction requires a level of carbon data reliability that has historically been missing from the market."

What’s the background?

Scope 3 emissions include indirect greenhouse gas emissions produced throughout a company’s value chain, making them difficult and costly for companies to measure and report. Many companies rely on estimates or industry averages when calculating these emissions.

Activist group disputes BP decision to exclude proposal

What’s the story?

Dutch activist shareholder group Follow This said it is considering legal options after BP declined to distribute a shareholder proposal the group submitted under the United Kingdom’s Companies Act. The proposal, filed in January and co-filed by investors managing more than €1 trillion in assets, asked BP to explain how it plans to create shareholder value if demand for oil and gas declines.

Follow This said BP initially confirmed the proposal met the requirements for submission but later rejected it on March 7, saying the resolution did not comply with the Companies Act or the company’s articles of association. BP said the board determined, after receiving legal advice, that the proposal did not meet legal requirements.

Follow This founder Mark van Baal said excluding the resolution could violate shareholder rights:

“BP’s refusal to bring a resolution to a vote is an attack on shareholder rights. Omitting a resolution that the company confirmed as valid may constitute a breach of its obligations under the UK Companies Act. We are pursuing all avenues to defend the rights of shareholders.”

What’s the background?

The proposal represents a shift in strategy for Follow This, which previously focused on asking oil companies to adopt emissions-reduction targets aligned with the Paris Agreement. The new resolution instead asks BP to disclose strategies for maintaining profitability as global energy demand potentially changes.

Follow This said it submitted a nearly identical proposal to Shell, which confirmed the resolution is valid and plans to include it for a vote at its annual general meeting in May.

The group has filed six shareholder proposals with BP, five of which previously went to a vote. Shareholders rejected a recent proposal 83%-17% in 2023, after BP’s board argued against it.

Study finds ESG funds still holding BP shares

What’s the story?

A Financial Times analysis found that BP’s decision to shift back toward oil and gas production has not led most large environmental, social, and governance (ESG) funds to sell their shares. Data compiled from Morningstar Direct, a fund-holdings database, showed that more than 110 ESG-labeled funds held BP at the end of 2025, including more than 60 actively managed funds that choose portfolio holdings rather than simply tracking an index.

BP had pledged in 2020 to transition toward lower-carbon energy and cut oil and gas production 40% by 2030, but the company announced a strategy reset in 2025, reducing that target to 25% after executives said the company had moved too quickly in shifting away from fossil fuels.

Several major asset managers that offer ESG funds — including BlackRock, UBS, and Legal & General — continue to hold BP despite the company reducing its planned cut to oil and gas production.

What are the arguments?

BP’s continued presence in ESG-labeled funds has fueled debate about how sustainability funds define their investment strategies. Some analysts say the holdings raise concerns about greenwashing, a term used to describe situations where companies or investment products promote environmental commitments that may not fully match their activities or investments.

Other asset managers say keeping shares in companies like BP allows them to influence corporate strategy through shareholder engagement. Rather than selling their positions, they say investors can use their voting rights and direct discussions with company leadership to encourage stronger emissions disclosures, transition planning, and other climate-related policies.