In this week’s edition of Economy and Society:

- Advocacy groups sue SEC over proxy policy shift

- Senators urge SEC to review Chinese market access

- EU states push to lift fossil fuel exclusions

- South Korea bill would mandate ESG in pension

- ESG legislation update

- Analysts say Vanguard settled to avoid antitrust test

In Washington, D.C.

Advocacy groups sue SEC over proxy policy shift

What’s the story?

On March 19, 2026, two investor advocacy groups — the Interfaith Center on Corporate Responsibility and As You Sow — filed a lawsuit in U.S.District Court for the District of Columbia challenging how the Securities and Exchange Commission (SEC) changed its handling of shareholder proposals. The groups said the SEC did not follow required rulemaking procedures under the Administrative Procedure Act (APA) when it altered its interpretation of Securities Exchange Act Rule 14a-8, which governs when companies can exclude shareholder proposals from proxy ballots.

The dispute centers on the SEC’s November decision to stop issuing no-action letters — guidance companies use to determine whether they can exclude shareholder proposals. The agency said the pause was due to time and resource constraints following a previous government shutdown. SEC Chairman Paul Atkins said the agency would use the current proxy season to evaluate whether to resume its role in reviewing these requests.

The groups argued the shift changed how Rule 14a-8 operates without formal rulemaking and could lead to more shareholder proposals being excluded from ballots.

Why does it matter?

The case focuses on how the SEC sets policy governing shareholder proposals and whether it must use formal rulemaking to change long-standing practices. A ruling against the agency could require it to restart the no-action process or adopt changes through notice-and-comment procedures.

The shift has also moved more disputes into courts. Investors have filed lawsuits to force companies to include proposals, including a case involving New York City pension funds and AT&T that ended in a settlement allowing a proposal to proceed.

What’s the background?

Rule 14a-8 allows shareholders to submit proposals for inclusion in company proxy statements and permits companies to request SEC staff confirmation that a proposal may be excluded. The SEC has historically provided that guidance through no-action letters indicating whether staff would recommend enforcement if a company omits a proposal.

In November 2025, the SEC’s Division of Corporation Finance said it would not respond to most no-action requests for the 2025–26 proxy season, limiting responses to certain state law questions. Atkins later said the change followed a 42-day federal government shutdown that left staff with a backlog of time-sensitive filings, including registration statements.

The APA generally requires federal agencies to follow notice-and-comment procedures when issuing or changing rules, though agencies may adjust internal practices or guidance without formal rulemaking.

Senators urge SEC to review Chinese market access

What’s the story?

Eighteen members of the Senate Banking Committee — 13 Republicans and five Democrats — sent a bipartisan letter on March 19, 2026, to SEC Chairman Paul Atkins urging the agency to review risks tied to Chinese companies accessing U.S. capital markets.

The committee members, led by Chairman Tim Scott (R-S.C.) and Ranking Member Elizabeth Warren (D-Mass.), said there are “unique risks to national security, market integrity, and investor protection posed by SEC-registered entities with ties to the People’s Republic of China.”

Lawmakers focused on variable interest entities (VIEs), warning that “American investors… will – sometimes unknowingly – purchase shares in an offshore shell company contractually tied to a PRC-based operating entity.” They said these structures can leave investors with “little or no meaningful legal protection” and limited ability to participate in corporate decision-making.

The committee asked the SEC to review whether disclosure rules and oversight tools adequately address these risks and whether additional safeguards are needed.

What’s the background?

The SEC’s Division of Corporation Finance has previously warned about risks tied to China-based issuers and VIE structures. In 2020 guidance, the division said limits on U.S. regulatory access may be materially limited, creating “substantially greater risk that their disclosures may be incomplete or misleading.”

The guidance also said that VIE arrangements can be less effective than direct equity ownership and may expose investors to penalties or loss of control if Chinese authorities determine the structure does not comply with local law. It further noted that investors may face limited legal recourse and difficulty enforcing claims against China-based companies.

These issues have informed ongoing regulatory and congressional attention to disclosure standards, oversight limits, and investor protections for foreign issuers in U.S. markets.

Around the world

EU states push to lift fossil fuel exclusions

What’s the story?

A group of European Union member states proposed removing fossil fuel exclusions from the Sustainable Finance Disclosure Regulation (SFDR), according to documents Responsible Investor reviewed. The proposal would change current rules that limit investment in companies expanding fossil fuel production or lacking plans to transition away from coal.

Under the European Commission’s framework, funds labeled as supporting climate transition strategies cannot invest in companies that are increasing fossil fuel activity or do not have coal phaseout plans. Member states discussed revising or removing those exclusions during a European Council working group meeting, with several countries raising concerns that the rules would discourage investment in energy companies during the transition.

Industry groups have also weighed in. The European Fund and Asset Management Association said as much as 95% of the global energy sector — and more than half of emerging market utilities — could be excluded from EU transition-labeled funds under the current framework.

Why does it matter?

The proposal highlights divisions within the EU over how environmental, social, and governance (ESG) investing rules should treat fossil fuel companies. Removing or revising the exclusions would allow more energy firms to qualify for ESG-labeled funds, expanding the pool of eligible investments.

At the same time, member states are considering stronger safeguards against greenwashing — when a company or financial product makes misleading or unsupported claims about its environmental practices or sustainability benefits. Draft proposals would require funds to demonstrate credible transition strategies, including defined targets, governance processes, and ongoing monitoring. These changes would affect how ESG funds are classified and marketed across the EU.

What’s the background?

The SFDR, in effect since 2021, sets disclosure requirements for financial products that promote ESG strategies or sustainability objectives. It created categories such as Article 8 funds, which promote environmental or social characteristics, and Article 9 funds, which have sustainability as a core objective.

The European Commission proposed updates to the SFDR on Nov. 20, 2025, to simplify disclosures and replace the Article 8 and 9 system with new categories, including Sustainable, Transition, and ESG Basics. The changes respond to concerns that existing rules are complex and have been used as labels rather than disclosure tools.

South Korea bill would mandate ESG in pension

What’s the story?

The Democratic Party of Korea is advancing legislation in the National Assembly that would require ESG factors to be considered in managing the National Pension Service fund, according to a March 23, 2026, report from Seoul Economic Daily. The proposal would amend the National Pension Act to change the governing language from may consider to shall consider, making ESG integration mandatory across the fund’s investment decisions.

The bill, introduced by Rep. Kim Yun, would also revise how external asset managers are selected and evaluated. In addition to financial returns, the process would incorporate qualitative factors such as fiduciary duty compliance, which would increase the role of ESG-related considerations. The legislation would also clarify that the Minister of Health and Welfare is responsible as a prudent manager overseeing the fund’s management and operations.

Why does it matter?

The National Pension Service manages approximately 1,400 trillion won (about $1.03 trillion) in assets, making it South Korea’s largest institutional investor. Requiring ESG consideration across the fund would formalize ESG as part of fiduciary decision-making rather than an optional factor and could influence how large public funds approach investment standards.

The proposal is part of a broader set of efforts by Democratic Party lawmakers to strengthen stewardship requirements in financial markets. A separate bill would require regulators to evaluate financial companies’ compliance with stewardship codes and disclose the results publicly.

In the states

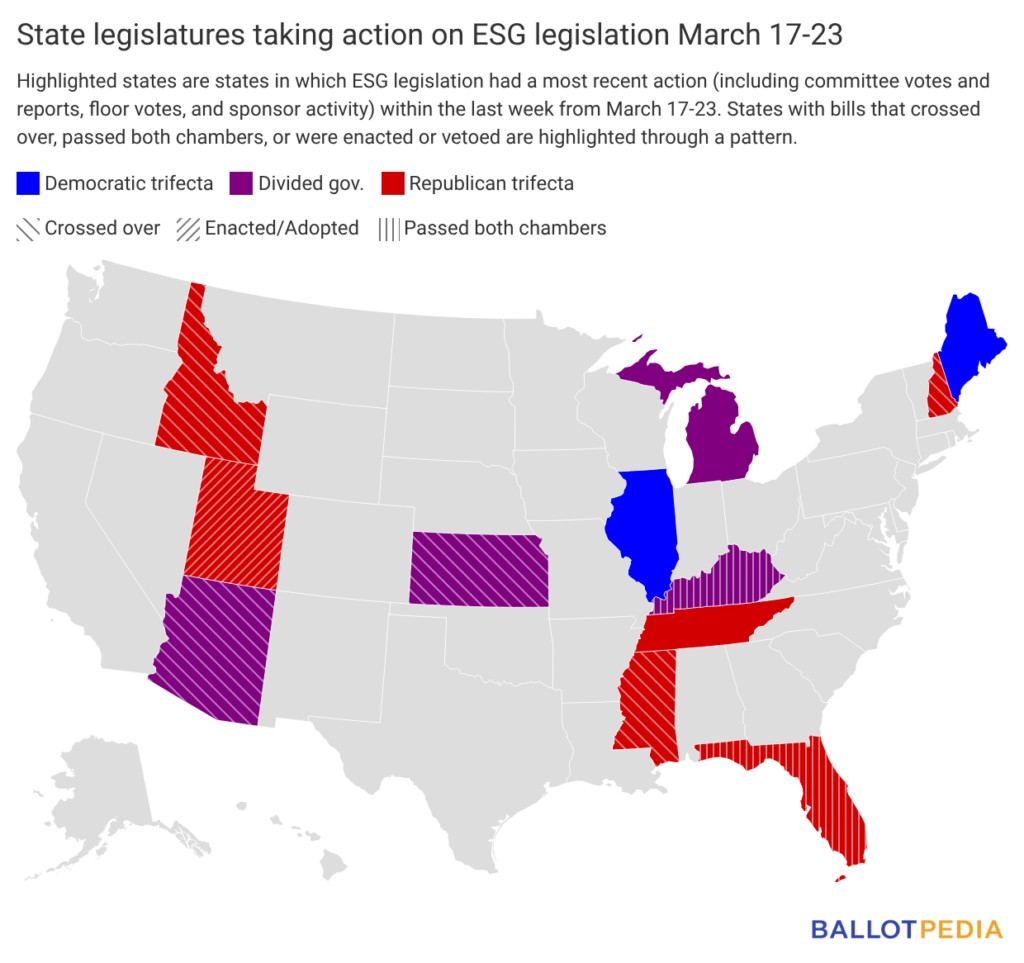

ESG legislation update

Twelve states took action on 18 ESG-related bills last week (since March 17, 2026). On March 17, 2026, Gov. Spencer Cox (R) signed Utah SB0298, prohibiting issuers of programmable money — digital currency that can include rules or conditions controlling how, when, or where it is spent — from restricting or denying transactions based on ESG-related criteria such as social credit scores, environmental standards, or DEI policies.

States with legislative activity on ESG last week are highlighted in the map below. Click here to see the details of each bill in the legislation tracker.

In the spotlight

Analysts say Vanguard settled to avoid antitrust test

What’s the story?

Two Heritage Foundation scholars said Vanguard’s decision to settle a Texas-led antitrust lawsuit may reflect legal risks tied to its passive investing model rather than litigation costs alone. In a March 20, 2026, commentary published by The Daily Signal, Stephen Soukup and Allen Mendenhall said a trial could have tested the common ownership theory, which examines whether large asset managers’ ownership stakes in competing firms reduce competition.

The lawsuit, led by Texas Attorney General Ken Paxton (R) and other Republican attorneys general, alleged Vanguard, BlackRock, and State Street coordinated pressure on coal companies to reduce output, which the states said increased electricity prices. Vanguard agreed to pay about $30 million and provide communications related to its ESG activities. The firm said it settled to avoid the burden and expense of continued litigation.

Soukup and Mendenhall wrote that the risks of going to trial extended beyond legal costs, arguing that the case could have challenged the foundations of passive investing:

After all, the firm agreed not only to pay almost $30 million in fines but also to turn over communications related to its ESG activities—a massive, potentially embarrassing and costly concession. The true 'costs' of letting this case reach trial, in other words, must have far exceeded the mere 'burden and expense of litigation.'

They said Vanguard’s business model makes it particularly exposed because nearly all of its roughly $12 trillion in assets under management are in passive funds.

In February 2026, Vanguard made a statement about the settlement:

We made the decision to settle the litigation filed by the Texas attorney general and other states with our investors’ best interest in mind as it allows us to put this distraction behind us and focus on what matters—giving our investors the best chance for investment success.

Why does it matter?

The commentary discusses legal issues raised in the ongoing case against BlackRock and State Street, which have not settled. A U.S. district court judge ruled on Aug. 1, 2025, that most of the states’ antitrust claims could proceed, allowing courts to continue considering whether the firms’ alleged coordination through climate-related investor activity violated competition laws.

The authors said a trial would test how passive investing interacts with competition, particularly whether holding large stakes across competing firms changes incentives in ways that affect market behavior. That question remains unresolved and could shape how regulators and courts evaluate ESG-related engagement by large asset managers.