In this week’s edition of Economy and Society:

- SEC moves to rescind 2024 climate disclosure rule

- Employee benefits chief says ESG investments will face scrutiny

- European Parliament proposes stricter rules for ESG fund labels

- EU proposes ESG reporting exemption for asset managers

- ESG legislation update

- Survey shows increasing support for ESG, declining allocation

In Washington, D.C.

SEC moves to rescind 2024 climate disclosure rule

What’s the story?

The Securities and Exchange Commission (SEC) submitted a proposal to rescind its 2024 climate-risk disclosure rule to the Office of Information and Regulatory Affairs on May 4, 2026. The rule never took effect because litigation paused its implementation shortly after adoption.

SEC staff is also preparing recommendations to the commission to rescind the rule at Chair Paul Atkins' direction. In a May 8, 2026, letter to the Eighth Circuit Court of Appeals, the SEC said it plans to reconsider the rules through notice-and-comment rulemaking and does not intend to renew its defense in court. The agency said staff has prepared recommendations to address commissioners' concerns that the rules exceed the commission's statutory authority and that costs outweigh benefits.

The SEC representative said that "the Commission is focused on returning the agency to its core mandate — in line with its legal authority — restoring a materiality-focused approach to securities regulation."

Why does it matter?

The rules would have required public companies to disclose:

- Climate-related risks that have materially affected or are reasonably likely to materially affect business strategy, results of operations, or financial condition

- Environmental governance processes

- Financial effects of severe weather events and other natural conditions in audited financial statements

- Scope 1 (direct) and Scope 2 (indirect) greenhouse gas emissions for certain companies

The rules did not require disclosure of Scope 3 emissions from supply chain partners, which were included in the proposed version.

The three current commissioners — Atkins, Mark Uyeda, and Hester Peirce — have all stated the rules extend beyond the agency's authority. Atkins and Peirce were appointed by President Donald Trump (R), while Uyeda was appointed by President Joe Biden (D). The commission currently has two vacancies.

What’s the background?

In March 2024, the commission voted 3-2 to adopt the rule, with then-Chair Gary Gensler supporting it and Commissioners Mark Uyeda and Hester Peirce voting against it.

Nine lawsuits challenged the regulations immediately after adoption. The SEC paused implementation on April 4, 2024, while the Eighth Circuit Court of Appeals reviewed the consolidated cases. After President Donald Trump (R) took office in January 2025, then acting chair Uyeda asked the court to delay arguments. Atkins directed staff to withdraw the SEC's defense in March 2025. In September 2025, the Eighth Circuit ordered the SEC to formally rescind, repeal, modify, or resume its defense of the rules.

The SEC’s move parallels broader Trump administration efforts to roll back climate- and ESG-related regulations that officials say exceed agencies’ statutory authority, including the EPA’s February 2026 repeal of the 2009 greenhouse-gas endangerment finding.

California has climate risk reporting requirements on its books, and New York is working to advance its own climate reporting law, meaning some companies could still face climate disclosure requirements at the state level even if the SEC rescinds its rule.

Employee benefits chief says ESG investments will face scrutiny

What’s the story?

Daniel Aronowitz, head of the Department of Labor's Employee Benefits Security Administration (EBSA), said May 8, 2026, at a conference on employee stock ownership plans that the agency will prioritize enforcement actions against asset managers focused on environmental, social, and governance (ESG) investing or diversity, equity, and inclusion (DEI) initiatives.

Aronowitz said the agency will investigate firms that act in bad faith to misappropriate assets to enrich themselves or pursue purposes unrelated to providing benefits to workers.

"To be clear, EBSA is focused on true bad actors. Criminals will be punished," Aronowitz said. "This would include disloyal pursuits of ESG or its sister acronym DEI.”

What’s the background?

EBSA enforces the Employee Retirement Income Security Act (ERISA), which governs private-sector retirement and employee benefit plans, including 401(k)s and pension plans. The agency investigates fiduciary violations, prohibited transactions, missing plan assets, and failures to properly manage retirement plans, typically through civil enforcement actions in federal court.

According to the Labor Department, EBSA closed hundreds of civil investigations in fiscal year 2025 and recovered $1.4 billion for plans, participants, and beneficiaries through settlements, corrective actions, and court judgments.

The second Trump administration has increased scrutiny of ESG and DEI-related investment practices. Trump (R) issued an executive order on Dec. 11, 2025, directing the Secretary of Labor to revise regulations and guidance regarding the fiduciary status of individuals who manage or advise on proxy voting and corporate engagement for retirement plans covered under ERISA. EBSA issued technical guidance in April 2026 confirming that proxy advisers can be fiduciaries under ERISA. The agency is also rewriting a Biden-era regulation that made it easier to include ESG-related investments on 401(k) plan menus.

Arguments that ESG and diversity violate ERISA duties of loyalty or prudence are increasingly appearing in private litigation. In 2025, U.S. District Court Judge Reed O’Connor found that American Airlines Inc. violated its fiduciary duties by allowing BlackRock to use proxy voting and shareholder engagement strategies tied to ESG objectives in the company’s 401(k) plan.

Around the world

European Parliament proposes stricter rules for ESG fund labels

What’s the story?

The European Parliament's Committee on Economic and Monetary Affairs released a draft report on April 28, 2026, proposing amendments that would tighten labeling and disclosure requirements for sustainable investment products under the Sustainable Finance Disclosure Regulation (SFDR).

Rapporteur MEP Gerben-Jan Gerbrandy filed the draft, which would require financial market participants to disclose a limited set of mandatory Principal Adverse Impact (PAI) indicators for products using the new SFDR categories. The indicators would allow investors to compare financial products within each category.

The committee also proposes that products referencing sustainability factors but not falling under one of the new EU categories must include a disclaimer. If passed, it would state that the product "does not meet the EU standards for defining sustainable financial products and protecting against greenwashing."

For the ESG Basics category, the committee proposes requiring products to eliminate at least 20% of the lowest-rated securities before claiming ESG outperformance against an investment universe or benchmark.

Why does it matter?

The European Parliament will use the draft report to define its negotiating position on the European Commission's proposed SFDR overhaul. The Commission proposed in November 2025 replacing the current system with three clearer categories: Sustainable, Transition, and ESG Basics.

The mandatory PAI disclosure would increase reporting and compliance requirements for asset managers that use EU sustainability categories and give institutional investors a clearer basis for due diligence. The disclaimer requirement would affect how funds are named, sold, and explained to retail investors.

The committee also proposes raising the safe harbor threshold for taxonomy-aligned activities from 15% to 20% for relevant Sustainable and Transition products. The draft states this condition is already met by 44.1% of current Article 9 funds.

What’s the background?

SFDR has been in place since 2021 and sets rules for how financial market participants disclose sustainability risks and product-level information. The current system uses Article 8 designations for products that promote environmental or social characteristics and Article 9 for products with a sustainable investment objective.

The Commission launched a comprehensive review in 2023 that found existing disclosures overly complex and susceptible to misinterpretation. Industry groups and regulators have said the Article 8 and Article 9 disclosures functioned as informal labels and created confusion in the market.

The committee expects to present the draft report toParliament's Economic and Monetary Affairs committee in June, with lawmakers scheduled to vote in mid-July. The draft sets the regulation to apply 24 months after entry into force.

EU proposes ESG reporting exemption for asset managers

What’s the story?

The European Commission proposed on May 7, 2026 exempting asset managers from ESG reporting requirements on assets they manage on behalf of clients.

The commission opened the proposal to public comment and set a deadline of June 3, 2026, for feedback. If the commission approves, the measure would amend the European Sustainability Reporting Standards and exempt firms managing investments on behalf of clients "without retaining risks or rewards of ownership" from providing data on those investments.

EU member states and lawmakers must still approve the proposal. The proposal is part of the EU’s broader effort to simplify reporting requirements and improve competitiveness.

Why does it matter?

The European Sustainability Reporting Standards provide detailed instructions for how companies should comply with the bloc's Corporate Sustainability Reporting Directive. The EU rolled back CSRD in 2025, removing more than 80% of companies originally in scope from compliance requirements.

Money managers have argued they should not have to disclose ESG data for assets they do not own. Proponents say the data is critical to understanding the industry's effects on areas such as climate and biodiversity.

Pierre Garrault, senior policy adviser at the European Sustainable Investment Forum, said "The sustainability performance of financial institutions cannot be credibly assessed without transparency on the assets they manage.”

In the states

ESG legislation update

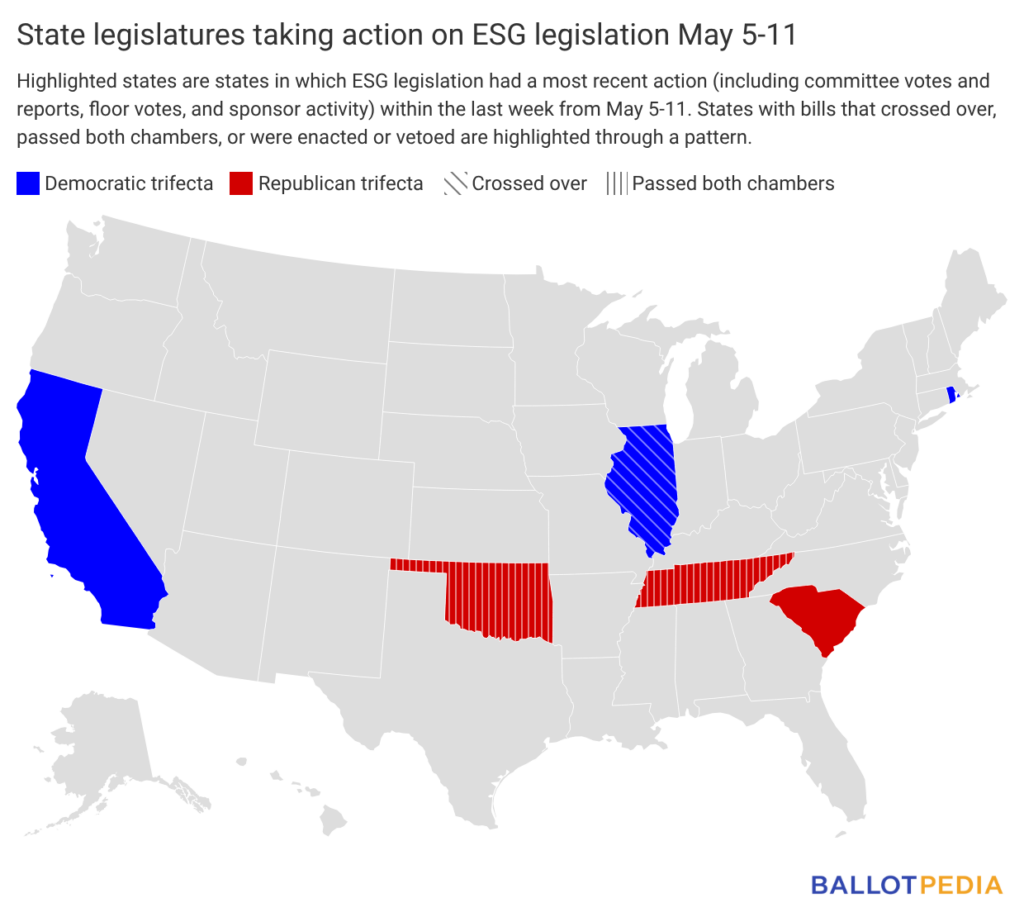

Six states took action on seven ESG-related bills since May 5, 2026.

States with legislative activity on ESG last week are highlighted in the map below. Click here to see the details of each bill in the legislation tracker.

On Wall Street and in the private sector

Survey shows increasing support for ESG, declining allocation

What’s the story?

The Morgan Stanley Institute for Sustainable Investing report released April 23, 2026, reveals that interest in sustainable investing among individual investors rose to 92% in 2026, up from 88% in 2025. The survey polled 2,250 active individual investors across North America, Europe, and Asia Pacific between February and March 2026. Three-quarters of respondents already hold portfolios with exposure to sustainable investments.

The report also found average portfolio allocation — the share of investors’ portfolios devoted to sustainable investments — fell slightly in 2026, declining to 31% from 33% in 2025. Morgan Stanley said the data suggests a disconnect between investor sentiment and allocation behavior.

Morgan Stanley's Chief Sustainability Officer, Jessica Alsford, said, "Our latest Sustainable Signals survey shows that performance continues to be the top driver of individual investors' interest in sustainable investing as they look to achieve both market-rate returns and real-world impacts."

Why does it matter?

Among investors interested in sustainable investing, 85% said their top reason was either support for real-world outcomes alongside market-rate returns or the expectation that sustainable investments may offer stronger returns than traditional peers.

Among the 64% of respondents planning to increase their allocation to sustainable investments over the next year, confidence in performance was the most common reason. The 5% planning to decrease their allocation cited weaker returns as the primary reason.

The survey found 64% of respondents see greater opportunity for sustainable investments in private markets than in publicly traded companies or instruments. Investors cited portfolio diversification, exposure to new technologies or business models, and access to high-growth investments as reasons. Three-quarters of global respondents either currently invest in private markets or plan to do so.

Greenwashing, when companies or investment products overstate or misrepresent their environmental or sustainability credentials, ranked as the top concern among investors, cited by 32%. Lack of transparency in data followed at 30%, while limited knowledge ranked third at 27%. In 2026, 25% of respondents rated barriers to sustainable investing as very significant, compared with 21% in 2025.

The survey also found 79% of respondents would select a financial advisor or investment platform based on its sustainable investing offerings.