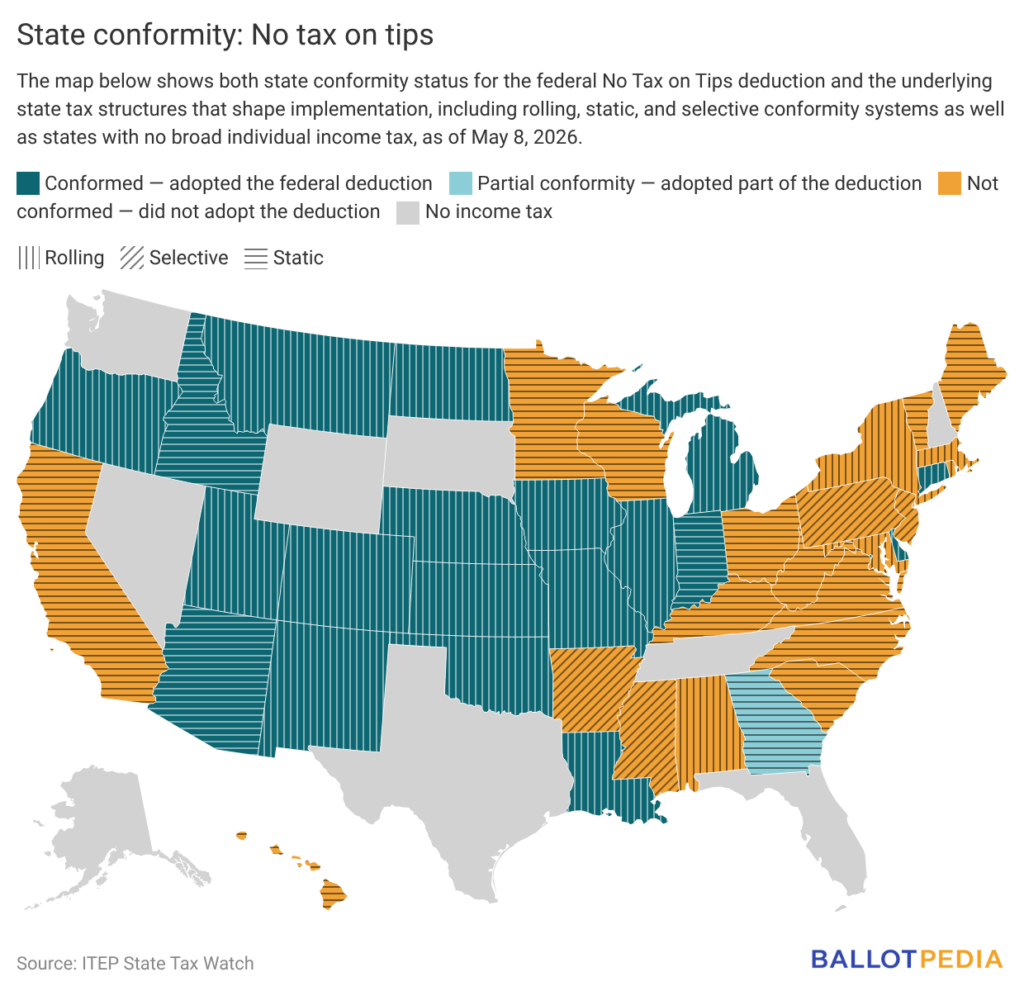

Of the 41 states that levy a broad individual income tax on wages, 19 conformed their tax codes to adopt the No Tax on Tips deduction created by the One Big Beautiful Bill Act (OBBBA) enacted on July 4, 2025. Twenty-one states have declined to adopt the deduction. Georgia has partially conformed to it.

The No Tax on Tips deduction allows eligible workers to deduct up to $25,000 in qualified tip income from their federal taxable income each year. It covers tax years 2025 through 2028.

Whether a state extends the No Tax on Tips deduction to its own income tax depends largely on how it conforms to the federal tax code.

State Conformity

States use one of three main approaches to conform their tax codes to federal law:

- States with rolling conformity automatically adopt most federal tax changes as they are passed, meaning a change takes effect at the state level without additional legislative action.

- States with static conformity tie their tax codes to the federal code as of a fixed date and do not automatically incorporate a provision passed after that date.

- States with selective conformity adopt federal provisions individually and must pass specific legislation to extend any given change.

The conformity method does not always determine the final outcome. Some rolling-conformity states passed legislation to specifically decouple from the federal No Tax on Tips deduction. Some static conformity states passed legislation to adopt it.

How the deduction Works

Tips must be voluntary and customer-determined. Automatic gratuities and mandatory service charges do not qualify. Cash tips are defined broadly to include payments by credit card, mobile app, gift card, and cash-equivalent tokens such as casino chips.

Workers must be employed in an occupation the Internal Revenue Service (IRS) has determined customarily and regularly received tips on or before Dec. 31, 2024. The IRS finalized regulations in April 2026 establishing a Treasury Tipped Occupation Code system covering more than 70 occupations across eight categories, including food and beverage service, hospitality, personal care, and transportation.

The deduction phases out at a rate of $100 for every $1,000 of modified adjusted gross income above $150,000 for single filers and $300,000 for joint filers. It does not affect payroll taxes. Tip income remains subject to Social Security and Medicare taxes.

Supporters say the deduction reduces the tax burden on service-industry workers. In an April 2026 press release, the Republican majority on the U.S. House Ways and Means Committee, chaired by Rep. Jason Smith (R-Mo.), said the provision "will cut taxes, on average, by $1,300 for tipped workers."

The Tax Foundation, a nonpartisan tax policy research organization, noted the proposal drew broad bipartisan public support, citing polling showing 73 percent of Americans backing the concept as relief for lower-wage service workers.

Critics have raised concerns about cost and scope. The Cato Institute wrote that the provision "reduces federal revenue by about $30 billion per year, or roughly 1.1 percent of total income tax receipts," and cautioned against the accumulation of targeted carve-outs in the tax code.

One Fair Wage, a labor advocacy organization, said the policy does not address underlying wage issues in the service industry, arguing that "ending income taxes on tips will not make subminimum wages livable."

In addition to the No Tax on Tips provision, Ballotpedia also has extensive coverage of the state implementation of the OBBBA’s Supplemental Nutrition Assistance Program (SNAP) provisions and the U.S. school choice tax credit scholarship program.