In this week’s edition of Economy and Society:

- SEC formally proposes rescinding Biden-era climate disclosure rule

- New York Governor Signs Budget Delaying Emissions Targets to 2040

- ESG legislation update

- Brazil shifts emissions reporting from mandatory to voluntary

- Exxon shareholders approve move to Texas despite proxy advisory opposition

In Washington, D.C.

SEC formally proposes rescinding Biden-era climate disclosure rule

What’s the story?

The Securities and Exchange Commission (SEC) formally proposed rescinding its 2024 climate-risk disclosure rule on May 29, 2026. SEC Chair Paul Atkins directed the proposal, which states that the 2024 rules are "a dramatic overreach of the Commission's statutory authority and, independently, unsound as a matter of policy."

The 2024 rule, adopted under then-Chair Gary Gensler, never took effect. The SEC paused implementation on April 4, 2024, shortly after adoption while the Eighth Circuit Court of Appeals reviewed nine consolidated lawsuits challenging the regulation.

Under the 2026 rescission proposal, the SEC would eliminate requirements for public companies to disclose climate-related risks with material impacts on business strategy, environmental governance processes, financial effects of severe weather and natural conditions, and Scope 1 and Scope 2 greenhouse gas emissions. Scope 1 emissions are direct emissions from company operations; Scope 2 are indirect emissions from purchased electricity.

Why does it matter?

Atkins argued the 2024 rules imposed substantial costs on companies and investors without justified informational benefits. He said "SEC disclosure obligations should comply with the Commission's statutory authority, be guided by materiality as the North Star, avoid the practical effect of dictating corporate behavior, and be imposed only when the expected benefits justify the likely costs and burdens."

Some environmental groups and investor advocates oppose the rescission. Director of Land Systems at Clean Air Task Force Kathy Fallon said the rule "was an important step toward giving investors consistent information about financially material climate risks."

Senior attorney for the Environmental Defense Fund Stephanie Jones said climate disclosure "makes sure people have information that they need to make important financial decisions," and the EDF stated it intends to "vigorously oppose rolling back the rule, which would threaten the financial security of workers and retirees who have their life savings invested in the markets."

What’s the background?

The SEC initially proposed climate disclosure requirements on March 21, 2022. On March 6, 2024, the SEC commissioners voted 3–2 along party lines to adopt the rule.

After President Donald Trump (R) took office in January 2025, the SEC reversed course. Acting Chair Uyeda asked the Eighth Circuit Court of Appeals to delay arguments in March 2025, and the SEC voted to end its defense of the rules on March 27, 2025. In September 2025, the Eighth Circuit ordered the SEC to formally rescind, repeal, modify, or resume defending the rules.

The notice-and-comment rulemaking process will remain open for 60 days after Federal Register publication.

In the states

New York Governor Signs Budget Delaying Emissions Targets to 2040

What’s the story?

Governor Kathy Hochul (D) signed New York's $268.5 billion fiscal year 2027 budget on May 28, 2026, including provisions that delay the state's emissions reduction targets by ten years. The budget law modifies the state's 2019 Climate Leadership and Community Protection Act (CLCPA).

Hochul and lawmakers replaced a requirement to achieve 40% emissions reductions by 2030 with a new target of 60% reductions by 2040, measured against 1990 baseline levels. The state's 2050 target of 85% emissions reductions remains unchanged.

Hochul and the legislature also pushed back the deadline for the New York Department of Environmental Conservation to adopt emissions reduction regulations to the end of 2028. The original 2019 CLCPA required regulations by 2024, a deadline the state missed. The New York Supreme Court, the state’s main trial court rather than its highest court, ordered the department to issue regulations by early 2026 unless the law changed.

Lawmakers also shifted how the state measures greenhouse gas emissions from a 20-year accounting standard to a 100-year standard and increased funding for disadvantaged communities, areas with disproportionate exposure to pollution and low-income concentrations, from 35% to 40% of climate investment benefits.

Why does it matter?

Hochul said, "New York has led and will continue to lead on clean energy and climate, but reality has been harsh. We cannot meet the current timelines without driving energy costs higher. The facts bear that out, and I cannot let that happen. We have to strike the right balance between our clean energy ambitions and the affordability pressures that real New Yorkers are facing right now."

New York Senate Finance Committee Chair Liz Krueger (D) disputed the cost rationale. Krueger said, "Those of us living in reality know that if we do what the governor is proposing and roll back CLCPA, it will do absolutely nothing to reduce energy costs for New Yorkers. The only problem it would solve is the manufactured political crisis that the governor has created for herself."

New York Senate Minority Leader Rob Ortt (R) called for repeal of the climate law entirely, saying "The only way to ensure affordable and reliable energy is to repeal the Climate Act and move forward with a new plan that is realistic."

What’s the background?

Lawmakers approved the CLCPA in 2019, establishing mandatory targets for New York to achieve 85% economy-wide emissions reductions by 2050, with an interim target of 40% by 2030. The law also required the state to meet 70% of electricity needs through renewable energy by 2030 and 100% zero-emissions electricity by 2040.

In March 2026, 29 Democratic state senators sent Hochul a letter stating they "categorically oppose any effort to roll back New York's nation-leading climate law."

According to the Climate Policy Dashboard, 25 states have adopted statewide greenhouse gas emissions reduction targets.

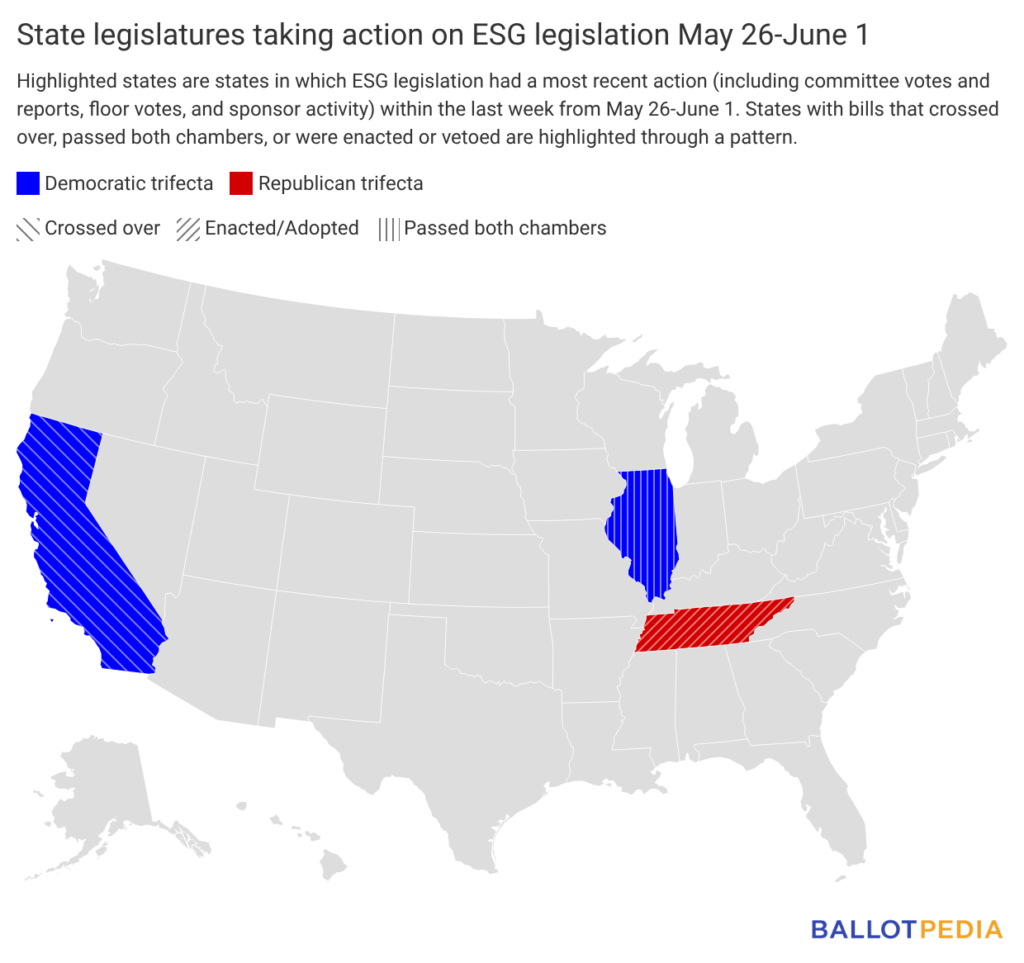

ESG legislation update

Three states took action on four ESG-related bills since May 26, 2026. Tennessee House Bill 2476, a companion bill to Senate Bill 2641, completed the legislative process after similar provisions were enacted through the Senate bill. The bill requires certain local public pension fiduciaries to make investment and proxy voting decisions solely for financial reasons and establishes related reporting and financial-analysis requirements.

States with legislative activity on ESG last week are highlighted in the map below. Click here to see the details of each bill in the legislation tracker.

Around the world

Brazil shifts emissions reporting from mandatory to voluntary

What’s the story?

Brazil's Securities and Exchange Commission (CVM) changed its sustainability reporting policies on June 1, 2026, moving from a mandatory to a voluntary emissions reporting for public companies. However, the CVM imposed a comply-or-explain requirement: companies that choose not to file sustainability reports must publicly announce their decision and explain their reasons when they submit financial statements in 2027.

In October 2023, the CVM originally approved mandatory International Sustainability Standards Board (ISSB) aligned emissions reports that all public companies were supposed to begin filing in 2026. Companies will now be able to opt out of sustainability reporting without penalty. For companies that proceed with reporting, they must follow ISSB standards and maintain reporting for at least three consecutive years. If a company stops reporting, it must disclose that decision in a market announcement the year before it stops.

The CVM said in its statement, "The changes aim to improve the voluntary adoption model, preserving the transparency and comparability brought about by the need to comply with accounting standards, but restoring the necessary respect for the freedom of entities to estimate the expected costs and benefits of their decisions on how to use investor resources."

Why does it matter?

The CVM's shift represents a retreat from Brazil's earlier commitment to mandatory climate disclosures. In October 2023, CVM President João Pedro Nascimento said, "We are the first regulator and country in the world to adopt sustainability reporting rules, following IFRS S1 and S2 standards."

The new change affects how much climate and sustainability information investors will receive from Brazilian public companies. Companies can defer or skip reporting costs that executives consider too high, potentially leaving investors with incomplete data about climate risks. The comply-or-explain approach means some companies will disclose why they are not reporting, but others may simply accept the cost of having to explain their choice rather than incur reporting expenses.

On Wall Street and in the private sector

Exxon shareholders approve move to Texas despite proxy advisory opposition

What’s the story?

Exxon Mobil shareholders approved the company's move from New Jersey to Texas on May 27, 2026, with 71.3% voting in favor of the move. More than 88% of outstanding shares were represented at the annual meeting.

Proxy advisory firms Glass Lewis and Institutional Shareholder Services (ISS) recommended shareholders reject the redomicile, citing concerns that the move could erode shareholder rights. The New York City Comptroller's office, which manages city pension funds, also opposed the redomicile.

However, the Big Three asset managers — BlackRock, Vanguard, and State Street — collectively own 22% of Exxon, and available evidence suggests all three voted in favor of the move. The three board members placed on Exxon's board in 2021 by investment firm Engine No. 1, which has pushed for climate-related governance changes at the company, also voted for the move.

Why does it matter?

Bloomberg Law analyst Michael Toth wrote that the vote "signal[s] that the major asset managers have turned the page on progressive-leaning corporate activism." The Big Three have scaled back environmental, social, and governance (ESG) commitments in recent years, with Vanguard refusing to divest from fossil fuel companies in 2022 and BlackRock removing diversity mandates from board-selection proxy voting analysis.

The vote demonstrates asset managers are less reliant on proxy advisory recommendations at a moment when both Republican officials and corporate executives are challenging the firms for allegedly using ESG and diversity, equity, and inclusion (DEI) factors in voting recommendations. Four Republican attorneys general sued ISS on May 20, 2026, alleging the firm misled investors, and the state has challenged both firms' recommendations on Texas-related proposals.

Derek Kreifels, CEO of Prospr Aligned and a former state financial officer who helped lead conservative opposition to ESG, wrote an op-ed in The Washington Examiner arguing shareholders prioritize financial returns over ESG objectives. He wrote: "The people who own U.S. companies, often indirectly through 401(k)s and pension funds, did not ask to be part of the ESG experiment. And when they are asked, as they increasingly are through ballot initiatives, state legislative sessions, and votes like the one at Exxon this week, the answer is a resounding no."