In this week’s edition of Economy and Society:

- Federal prosecutors subpoena banks over alleged closure of accounts

- S&P launches UN Global Compact screening tool

- SBTi releases updated corporate net-zero standard

- ESG legislation update

- No ESG-related shareholder proposals pass in 2026 proxy season

In Washington, D.C.

Federal prosecutors subpoena banks over alleged closure of accounts and denial of services

What’s the story?

According to reporting from The Wall Street Journal, the U.S. Attorney’s Office in Washington, D.C. has subpoenaed major banks as part of investigations into the alleged closure of accounts and denial of services, or debanking. According to the Trump administration:

The term ‘politicized or unlawful debanking’ refers to an act by a bank, savings association, credit union, or other financial services provider to directly or indirectly adversely restrict access to, or adversely modify the conditions of, accounts, loans, or other banking products or financial services of any customer or potential customer on the basis of the customer’s or potential customer’s political or religious beliefs, or on the basis of the customer’s or potential customer’s lawful business activities that the financial service provider disagrees with or disfavors for political reasons.

The office of U.S. Attorney Jeanine Pirro sent subpoenas to banks including JPMorgan Chase, Bank of America, and Wells Fargo. The subpoenas, some of which date to 2025, asked the banks to provide a list of accounts subject to alleged debanking and to provide an explanation for the closure of any accounts. According to The Wall Street Journal, prosecutors are looking into whether closures may have violated the Financial Institutions Reform, Recovery and Enforcement Act of 1989, a federal law that strengthened bank-fraud penalties in the wake of the savings and loan crisis.

The Wall Street Journal’s sources said that investigation began independently from similar investigations at the Office of the Comptroller of the Currency (OCC) which had not yet resulted in a referral for prosecution to the Justice Department.

What’s the background?

In August 2025, President Donald Trump (R) signed an executive order directing federal banking regulators to investigate what it called debanking and to “develop a comprehensive strategy for further measures to combat politicized or unlawful debanking.”

Trump said, “The banks discriminate against conservatives, they discriminate against religion, because they’re afraid of the radical left, I suspect. I think the bank regulators are doing a big number of the banks because they’re not allowed to do business with you. And we’re going to get those banks when we get in office.”

The order directed federal regulators to conduct a review of financial institutions within their regulatory jurisdiction to identify whether they “have had any past or current, formal or informal, policies or practices that require, encourage, or otherwise influence such financial institution to engage” in debanking, and to impose disciplinary measures as applicable by law.

The OCC, which regulates the nation's largest banks, has been the primary entity conducting this review. In December 2025, they released a preliminary report which found that “between 2020 and 2023, the [nine largest banks under its supervision] maintained public and nonpublic policies restricting certain industry sectors’ access to banking services, including by requiring escalated reviews and approvals before providing access to financial service.”

The report pointed to ESG or other social or corporate risk policy frameworks published during this time period, but did not contain specific details of alleged debanking. The OCC has not announced any disciplinary action, but has issued guidance for financial institutions on how to avoid unlawful debanking.

On Wall Street and in the private sector

S&P launches UN Global Compact screening tool

What’s the story?

In June, S&P Global Sustainable1, a unit of S&P Global, launched a new dataset designed to screen for corporate compliance with the United Nations Global Compact (UNGC). The UNGC is a voluntary corporate sustainability project started in 2000 in which companies commit to operating sustainably across four primary fields: human rights, labor, environment, and anti-corruption. The new tool identifies potential misalignment with the compact’s principles covering an initial list of 16,500 companies that will expand to 24,000.

Why does it matter?

According to S&P, the UNGC Screening Dataset is aimed at investment managers, bankers and non-financial corporates and “utilizes proprietary AI and machine learning models to systematically identify, classify, and quantify ESG and business risks.”

It provides two primary streams of evidence: controversy screening, which “(t)racks corporate controversies linked to one or more UNGC principles,” and business involvement screening, which “(f)lags corporate revenues originating from specific controversial products.”

Thomas Yagel, head of Sustainable1, said the dataset provides “clear and actionable UNGC alignment labels, enabling investors to integrate S&P Global Sustainable1 insights into their decision-making, portfolio construction and ongoing risk oversight.” A white paper published alongside the launch found that misalignment with standards was most frequently related to human rights violations/controversies.

S&P said that the UN had not reviewed or endorsed the tool.

What’s the background?

S&P’s dataset serves a market for sustainability reporting with demand largely centered in the European Union, where regulations create legal obligations for screening.

The EU’s Sustainable Finance Disclosure Regulation (SFDR) requires financial products that claim to promote environmental or social characteristics to disclose how they comply with UNGC principles, and requires fund managers to disclose UNGC misalignment or lack of tracking among their investments. The EU’s Corporate Sustainability Reporting Directive (CSRD) also establishes compliance reporting requirements, and some member states, such as France, have adopted these requirements into national law with penalties. In this way, EU policy does not directly require compliance with UNGC principles, but does require reporting on alignment.

Click the links to read more about the SFDR and CSRD.

SBTi releases updated corporate net-zero standard

What’s the story?

The Science Based Targets initiative (SBTi), which described itself as "a corporate climate action organization that enables companies and financial institutions worldwide to play their part in combating the climate crisis," released version 2.0 of its comprehensive Corporate Net-Zero Standard.

SBTi uses the Standard to validate companies that meet climate targets the organization defines as science-based. The new version introduces more flexibility for companies in setting near-term decarbonization goals and long-term transition plans.

Why does it matter?

A key change in the new Standard is the introduction of a new best efforts framework, which will allow corporations to explain how circumstances beyond their control have hindered their progress toward achieving their decarbonization goals. According to the organization’s chief executive, David Kennedy, companies will be expected to “deploy every lever within [their] control, be transparent about where barriers have limited what was possible, and demonstrate what [they] are doing to address those barriers over time.”

The update also changes requirements for companies based on size and national incomes. For example, they exempt small companies and medium-sized companies from lower-income countries from setting near-term targets for the reduction of Scope 3, or indirect emissions.

According to SBTi, the updated Standard “is designed to help companies strengthen implementation, demonstrate progress, and maximize the business value of decarbonization, while maintaining scientific rigor and ambition.”

What’s the background?

The SBTi launched its first Corporate Net-Zero Standard in 2021. In April 2026, SBTi announced that the number of companies with validated science-based climate targets had passed 12,000, with 2,800 validated in 2025.

SBTi's influence has attracted legal scrutiny from Republican state officials who argue the organization's practices raise antitrust and consumer protection concerns. On July 28, 2025, Florida Attorney General James Uthmeier (R) announced an investigation into SBTi and the Climate Disclosure Project (CDP), alleging deceptive trade practices and potential antitrust violations related to how companies set and report climate targets. In August 2025, 23 Republican attorneys general, led by Iowa Attorney General Brenna Bird (R), sent a letter to the organization requesting information about its standards.

Read more about SBTi here.

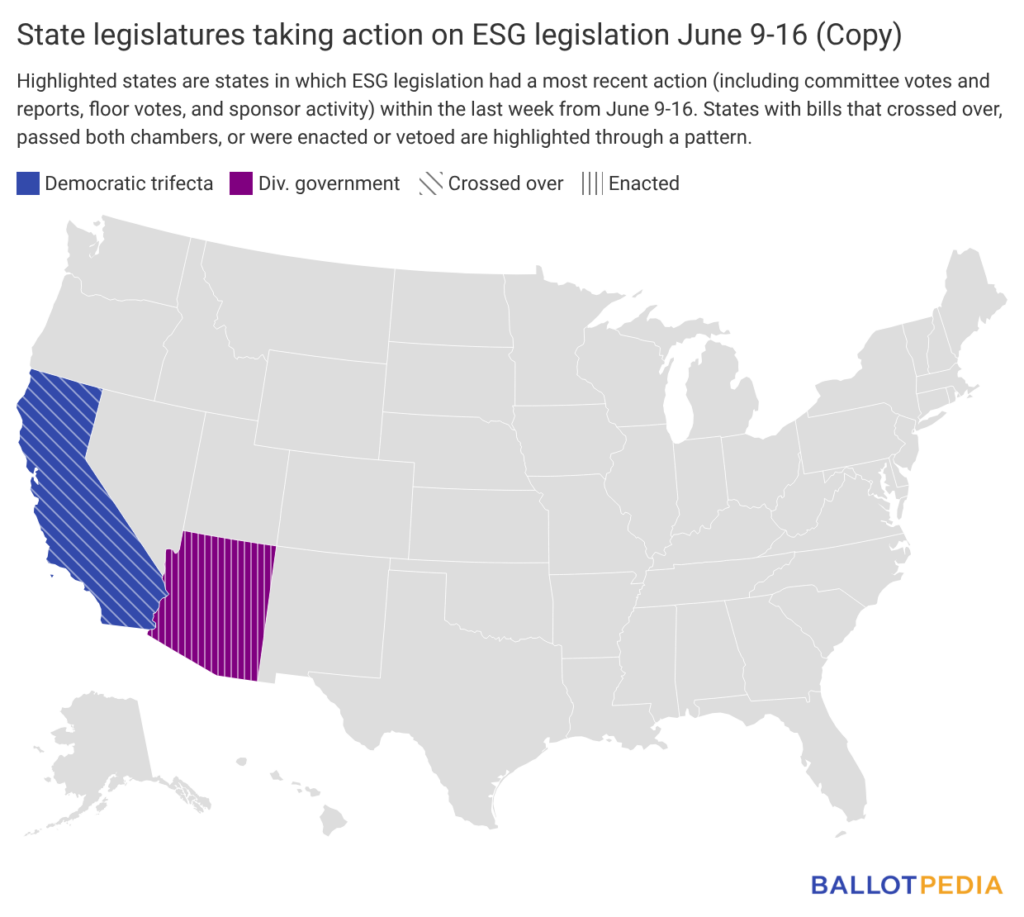

ESG legislation update

Two states took action on two ESG-related bills since June 9, 2026:

- Arizona’s HCR 2044 passed the legislature and referred a constitutional amendment to voters that, if approved, would prohibit the state from requiring DEI-related support or applying race-based preferences in public contracting, public employment, or public education. It passed along party lines with Republicans in support and Democrats opposing.

- California’s AB 2599, which passed the lower chamber, would require some companies, including financial and insurance companies, to disclose under penalty of perjury any business records related to slavery or human trafficking. It would make these disclosures publicly available on a digital platform. It passed along party lines with Democrats in support and Republicans opposing.

States with legislative activity on ESG last week are highlighted in the map below. Click here to see the details of each bill in the legislation tracker.

In the Spotlight

No ESG-related shareholder proposals pass in 2026 proxy season

What’s the story?

As of May 31, shareholders did not approve any proposals either in favor of or opposition to ESG-related topics during the 2026 proxy season. That’s according to a report summarizing the 2026 shareholder season published by the Harvard Law School Forum on Corporate Governance which identified 135 ESG-related proposals that shareholders voted on.

Why does it matter?

The report found that around 38% of the 135 proposals were anti-ESG and received an average vote in favor of about 1.7%. On the other side, 62% of proposals supported ESG-related actions or disclosures and had an average vote in favor of about 13.3%. A pro-ESG climate-related proposal received the most support of any of the proposals, but still failed to pass with 47% support.

Among anti-ESG proposals, the report found that:

This proxy season, proposals seemed to focus on three main areas: risk of negative impacts of certain charitable giving, risk of misalignment between a company’s values and those of its customers or viewpoint discrimination against customers, and risks of religious discrimination against employees.

The 2026 shareholder season also brought a rise in anti-ESG proposals related to healthcare and reproductive rights (13% of anti-ESG proposals), such as asking companies about risks related to distributing mifepristone or related to providing gender-affirming care within employee benefits packages.

In total, three shareholders were responsible for more than 60% of the anti-ESG proposals in 2026. The report concluded that shareholder support for anti-ESG proposals remains low, but that it appears “activist shareholders view these proposals as a way to draw attention to their views and objectives, even in the absence of widespread support.”

What’s the background?

The 2026 shareholder voting season is the first since a Securities and Exchange Commission (SEC) decision to not provide substantive guidance on the exclusion of shareholder proposals from proxy ballots under the Securities Exchange Act of 1934.

The change shifted more responsibility for exclusion decisions from SEC staff to companies. Instead of receiving the agency’s usual no-action responses, companies had to decide for themselves whether proposals could be omitted from proxy materials under SEC rules.

A mid-season analysis by Glass Lewis, a proxy advisory firm, found that companies are excluding significantly fewer shareholder proposals in 2026. As announced, the policy change applied only to the 2025-2026 proxy season.

A report from Root Intelligence found that the number of ESG-related proposals peaked at 322 in 2023. Support for pro-environmental and social proposals peaked in 2021, according to Institutional Shareholder Services. Shareholders have never approved an anti-ESG proposal according to the Harvard Law School Forum on Corporate Governance,

Read more about shareholder voting here.