Welcome to the Monday, June 22, 2026, Brew.

By: Briana Ryan

Here’s what’s in store for you as you start your day:

- State legislative incumbents are retiring at a lower rate, facing primaries at a higher rate in 2026

- U.S. Treasury previews guidance for federal Education Freedom Tax Credit scholarship program

- Rhode Island voters will weigh in on five bond issues in Nov. 2026 included in the state's budget

State legislative incumbents are retiring at a lower rate, facing primaries at a higher rate in 2026

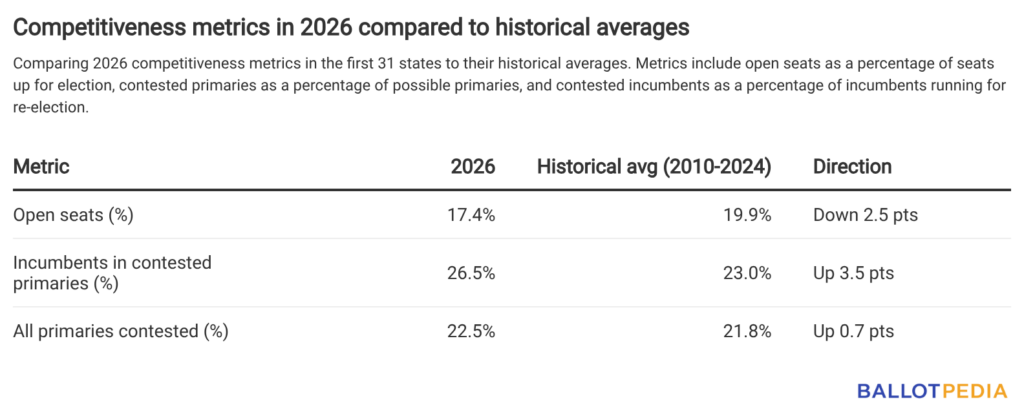

In the 31 states where we have completed an analysis of all the available candidate filing data for state legislative elections, an average of 26.5% of incumbent state legislators are running in contested primaries this year — the second-highest since 2010. The 17.4% average of open seats is the second-lowest since 2010.

The chart below shows three patterns that have emerged in those 31 states across even-year cycles since 2010:

Here's a closer look at what's driving these trends.

Percentage of incumbents facing primary challengers

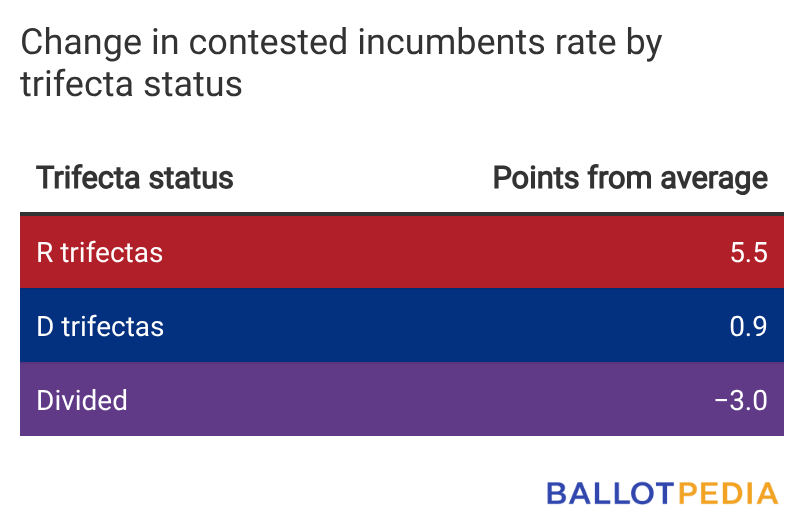

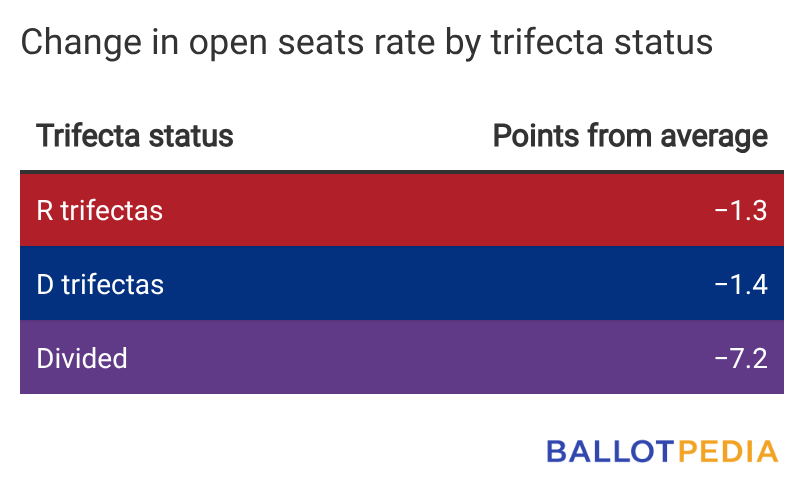

A larger share of incumbents face primary contests on average this year compared to previous years. That’s largely due to an increase in the percentage of contested incumbents in Republican trifecta states, up 5.5 percentage points from the 2010 to 2024 average. Meanwhile, incumbent contests are up less than one point in Democratic trifecta states and down three points in states with divided governments.

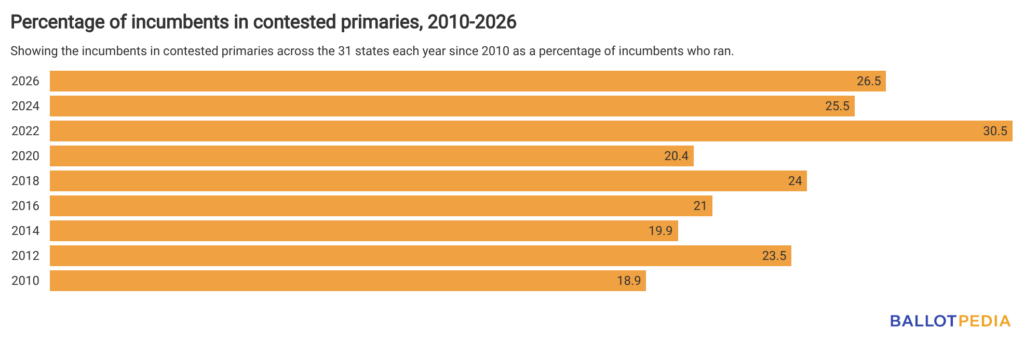

Between 2010 and 2024, an average of 23% of incumbents in the 31 states had primary challengers in each election. In 2026, an average of 26.5% of incumbents are running in contested primaries, second only to 2022, which saw 30.5%.

Nineteen states are above their own historical averages for contested incumbents this year, with 11 states more than five percentage points above average. The biggest jumps occurred in Indiana (+10 points), New York (+12 points), North Dakota (+22 points), Oklahoma (+14 points), Oregon (+13 points), and South Dakota (+38 points).

Twelve states have below-average incumbent contest rates this year, seven of which are more than five percentage points below average. The biggest drops occurred in Maryland (-16 points) and Michigan (-15 points).

Open seats, or incumbents not running for re-election

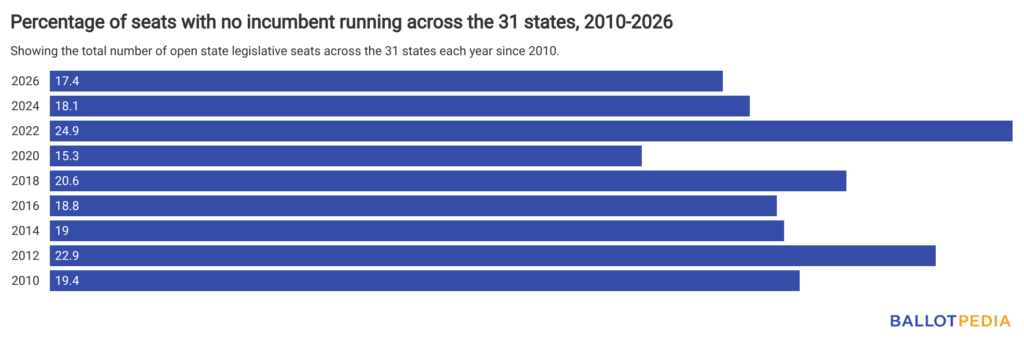

Across the 31 states, an average of 17.4% of state legislative seats up for election this year have no incumbent running. That's down from the historical average of 19.9%, and the second-lowest since 2010. Only 2020 was lower, with 15.3%. Twenty-two of the 31 states are below their own historical average for open seats.

The 31-state set includes 17 Republican trifectas, eight Democratic trifectas, and six divided governments. Open seats are down across all three categories, with the largest average declines occurring in states with divided governments.

Nevada, which has a divided government, had the largest decline in share of open seats, down 13 percentage points from its historical average. Nine states buck the trend and show increases in open seats this year. In four of those states, the share of open seats is five percentage points or more above average — Maine (+10 points), Nebraska (+8 points), North Dakota (+7 points), and Texas (+5 points).

Percentage of primary elections with more than one candidate

This year, an average of 22.5% of possible primaries are contested across the 31 states, 0.7 percentage points higher than the historical average of 21.8%.

While the states are not far from the average number of contested primaries collectively, there are a handful of noteworthy up- and downswings.

Three states are running more than eight percentage points above average: Indiana (+10 points), North Dakota (+9 points), and South Dakota (+14 points). Two states are running more than eight percentage points below average: Maryland (-11 points) and Michigan (-10 points).

Contested primaries also increased primarily among Republican trifecta states, where the share of primaries with more than one candidate are up almost three percentage points on average. Contested primaries are down one percentage point on average in Democratic trifecta states and down four percentage points in states with divided governments.

Click here to see our analysis of primary election competitiveness in state and federal government this year.

U.S. Treasury previews guidance for federal Education Freedom Tax Credit scholarship program

On June 10, the U.S. Department of the Treasury issued a preview of forthcoming guidance implementing the Education Freedom Tax Credit (EFTC) scholarship program, which is set to take effect on Jan. 1, 2027. The One Big Beautiful Bill Act (OBBBA) enacted the tax credit, which President Donald Trump (R) signed on July 4, 2025. The statute requires the U.S. Treasury to create regulations to implement the program, which department officials said they will issue in September.

The EFTC is a nonrefundable tax credit, allowing individuals to receive federal tax credits for donations up to $1,700 to authorized scholarship-granting organizations (SGOs). It is a dollar-for-dollar nonrefundable tax credit, meaning individuals can lower their federal tax liability by $1 for every $1 donated to accredited SGOs.

SGOs distribute donated scholarship funds to eligible families for a variety of private or public educational expenses, including private school tuition, tutoring services, textbooks, and more. To qualify for scholarships, students have to live in households earning no more than 300% of the area's median gross income (AGMI) and be eligible to enroll in K-12 schools. The program will take effect Jan. 1, 2027.

States that elect to participate must submit a list of SGOs that taxpayers can donate to in order to receive the federal tax credit. Students in states that do not opt in cannot receive scholarships funded under the program, but donors in those states can still receive a federal tax credit by donating to SGOs in participating states. As enacted, the program will not affect state budgets.

The June 10 preview addressed several key policy questions about the program.

- SGOs must spend 90% of their income on scholarships to participate in the tax credit. However, some SGOs would be able to have what the U.S. Treasury called a safe harbor account dedicated to funds under the program that could qualify as the SGO's income for the program's purposes.

- SGOs must be authorized to do business in a state that has opted into the scholarship program, and the Treasury Department will create a way for SGOs operating in multiple states to participate.

- Families will be able to use scholarships for both public and private school expenses, as well as homeschool expenses in states that treat them as schools under the law. The guidance did not address micro-schools.

- SGOs will have to verify a student's household income to determine their eligibility.

- The Treasury Department will issue guidance separate from the forthcoming September guidance regarding eligible expenses.

Zooming out

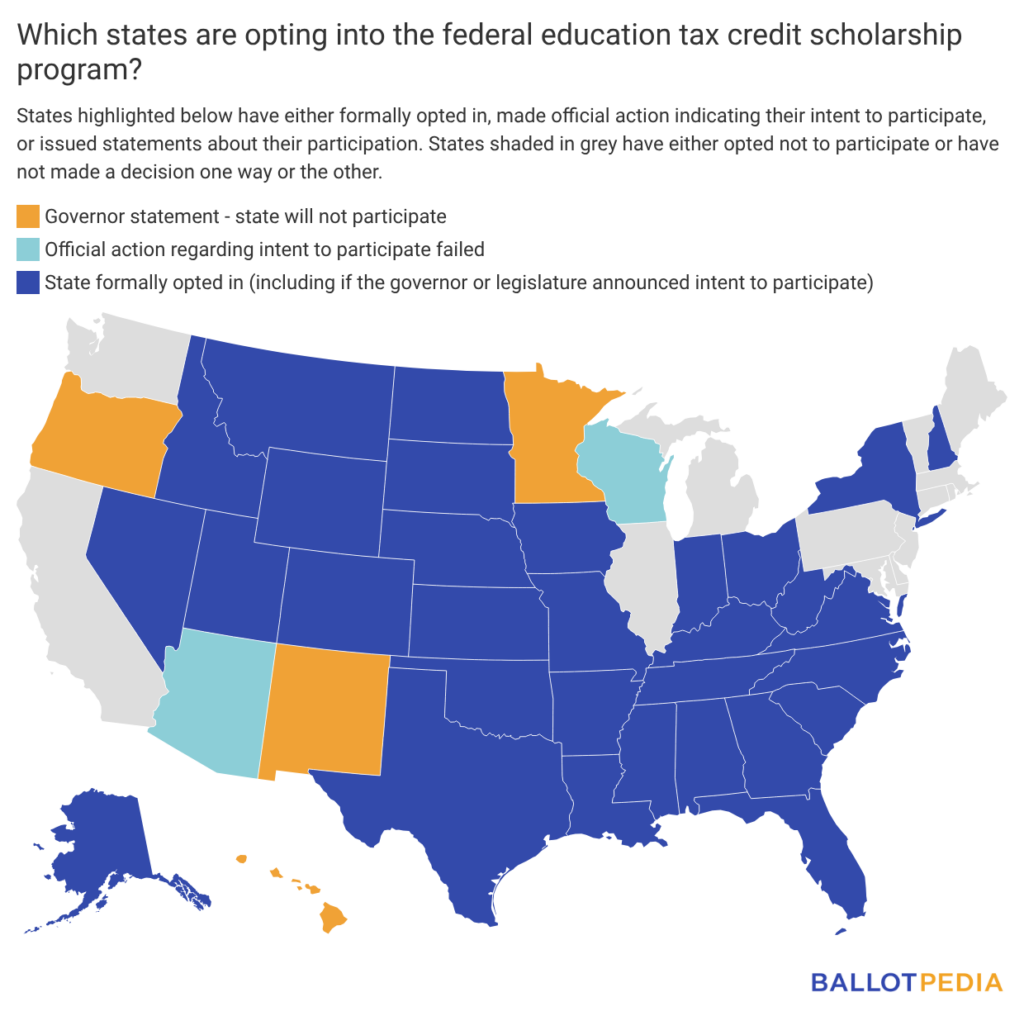

According to EducationWeek, governors of several Democratic states said they are waiting for the Treasury to issue guidance before deciding whether to participate in the program, even after the June 10 preview. On June 12, Gov. Tina Kotek (D) said Oregon would not participate in the program after reviewing it.

As of June 15, 31 states have either opted in to the program or indicated that they plan to.

Partisan breakdown of states that have indicated participation

- Six have Democratic trifectas. Virginia, Colorado, and New York have said they will participate in the program. Hawaii, New Mexico, and Oregon have said they would not participate, though all three governors of those states are reconsidering participation, according to EducationWeek.

- Twenty-three have Republican trifectas. All twenty-three states — Alabama, Arkansas, Florida, Georgia, Idaho, Indiana, Iowa, Louisiana, Mississippi, Missouri, Montana, Nebraska, New Hampshire, North Dakota, Ohio, Oklahoma, South Carolina, South Dakota, Tennessee, Texas, Utah, West Virginia, and Wyoming — said they would participate in the program.

- Eight have divided governments. The Republican-controlled legislatures in Kansas, Kentucky, and North Carolina overrode their Democratic governors' vetoes of bills requiring the state to opt into the program. In Arizona and Wisconsin, legislation to indicate participation failed. Alaska and Nevada formally opted into the program. Minnesota Gov. Tim Walz (D) said in March 2026 that the state would not participate in the program.

Click here for more information about the program.

Rhode Island voters will weigh in on five bond issues in Nov. 2026 included in the state's budget

Rhode Island voters will decide on five bond issues in the November 2026 election accounting for $600 million in general obligation bonds. The bond issues would fund housing development, higher education facilities, economic infrastructure development, environmental protection, and historical preservation.

In Rhode Island, the Legislature can place bond measures on the ballot with a simple majority vote in both chambers, and the governor must sign the bill to certify it.

Between 2000 and 2025, 58 bond measures have been on the ballot in Rhode Island. Voters approved 52 and rejected six.

Bond measures have been on the ballot in Rhode Island in every even-numbered year since 2000, except for 2020. Due to a delay in the approval of the 2021 budget, bond measures included in the budget bill were placed on the 2021 ballot instead. On average, in years when Rhode Island voters decided on bond measures, more than four were on the ballot.

The five bond measures were included in the state’s budget for the 2027 fiscal year, titled House Bill 7127 (H. 7127). Governor Dan McKee (D) signed the budget into law on June 12, after the state House passed it 65-10 and the state Senate passed it 31-7. Rhode Island has a Democratic trifecta.

While the five bond measures were all included in one bill, H. 7127, Rhode Island voters will decide on each measure independently.

The five bond measures are:

Higher Education Facilities Bond Measure – $275 million in bonds to fund the construction of:

- a new integrated health building for the University of Rhode Island;

- a workforce innovation center at the Community College of Rhode Island, Warwick campus; and

- a student success and career readiness center at Rhode Island College.

Housing Development Bond Measure – $120 million in bonds to fund the construction and development of residential accommodations to “increase and preserve the availability of affordable and accessible housing.”

Economic and Infrastructure Development Bond Measure – $100 million in bonds to fund infrastructure and economic development projects, including:

- industrial site selection, land acquisition, and preparation;

- infrastructure improvements and investments in the Quonset Business Park;

- project investments in the I-95 district;

- infrastructure to support Rhode Island’s ocean industries; and

- investments to advance job growth in the life sciences.

Environment and Watershed Protection and Development Bond Measure – $55 million in bonds to fund environmental preservation and water infrastructure projects, including:

- financial assistance for local water infrastructure improvements;

- the renovation, repair, and construction of existing and new recreational facilities; and

- the restoration and water quality protection of the Narragansett Bay.

Historical Center and Cultural Grants Bond Measure – $50 million in bonds to fund matching grants administered by the Rhode Island Historical Preservation and Heritage Commission and the construction of a new Rhode Island State History Center.

Click here to read more about these measures.