In this week’s edition of Economy and Society:

- Church of England fund to oppose bank directors

- California proposes phased Scope 3 emissions reporting

- ESG legislation update

- BlackRock CEO doesn't mention ESG in annual letter

- Companies split on ESG proposal lawsuits

- ESG funds shrink despite rising asset values

Around the world

Church of England fund to oppose bank directors

What’s the story?

On March 24, 2026, the Church of England Pensions Board (CEPB) said that it will vote against directors at banks it said have materially backtracked on climate commitments during this year’s annual general meeting (AGM) season. The board, which oversees £3.5 billion in assets, plans to vote against directors at NatWest, Santander, and HSBC and will review other banks as proxy voting continues.

CEPB said it will target directors responsible for weakened climate or risk policies and escalate votes against board chairs or members of sustainability or risk committees when governance concerns arise. The board treats climate change and nature loss as systemic risks, meaning risks that could affect the broader financial system rather than a single company.

Managing Director Laura Hillis said, “Investors need confidence that directors will maintain consistent, credible oversight of climate and risk policies. Where that confidence is undermined, we will act.”

Why does it matter?

Voting against directors is one of the most direct actions investors can take during proxy season, when shareholders vote on corporate leadership and governance. Pension funds use these votes to signal concerns about how companies manage financial risks, including risks tied to climate policy changes. The Church of England’s approach treats climate policy as a core financial risk issue tied to board oversight and long-term performance.

The board said weakening climate policies can raise concerns about oversight, risk management, and long-term resilience.

What’s the background?

Large banks have developed climate-related strategies in recent years, often including targets to reduce financed emissions — the greenhouse gas emissions tied to lending and investment activity.

- NatWest plans, in its 2025 Climate Transition Plan Report, to reduce the climate effect of its financing activity by 2030 compared with a 2019 baseline, while updating how it supports clients across sectors.

- Santander said in its 2025 sustainability presentation that it has set climate targets in the business areas where it says it has the greatest potential effect, while disclosing financed emissions for several lending portfolios.

- HSBC said it updated its Net Zero Transition Plan in November 2025 and revised its interim 2030 financed emissions targets.

In the states

California proposes phased Scope 3 emissions reporting

What’s the story?

The California Air Resources Board (CARB) on March 23, 2026, presented three options for how companies would report Scope 3 emissions — indirect greenhouse gas emissions from a company’s value chain, such as suppliers, transportation, and product use — under California’s corporate climate disclosure law, SB 253.

CARB shared the proposals during a public workshop on the state’s greenhouse gas reporting program and requested public comment through April 13.The agency said companies must begin reporting Scope 1 and Scope 2 emissions — direct emissions and emissions from purchased energy — by Aug. 10, 2026, with Scope 3 reporting scheduled to begin in 2027.

CARB outlined three approaches for Scope 3 reporting:

- Broad applicability: All covered companies would report all value-chain emissions categories beginning in 2027, with limited exceptions for emissions considered minimal.

- Sectoral phase-in: Transportation and industrial companies would report first, with other sectors added over time.

- Category phase-in: All companies would begin by reporting commonly tracked categories, including business travel, purchased goods and services, fuel- and energy-related activities, employee commuting, and operational waste.

CARB also described three methods for calculating emissions:

- Spend-based: Estimates emissions using the cost of purchased goods and services

- Activity-based: Uses physical measures, such as quantities purchased

- Supplier-specific: Uses emissions data reported directly by suppliers

The agency said companies could use any method or combine approaches. CARB also estimated compliance costs would range from about $135,000 to $152,000 annually per company, depending on the reporting approach.

CARB shared the proposals during a public workshop on the state’s greenhouse gas reporting program and requested public comment through April 13.

Why does it matter?

CARB’s proposals address one of the most complex parts of climate disclosure rules. Scope 3 emissions often make up most of a company’s total emissions but occur outside their direct control, which makes them harder to measure and verify.

What’s the background?

California has taken a leading role in corporate climate disclosure policy. Lawmakers passed SB 253 in October 2023, requiring companies with more than $1 billion in annual revenue that do business in the state to report greenhouse gas emissions annually. CARB adopted implementing regulations in February 2026 and set initial reporting deadlines for 2026 and 2027.

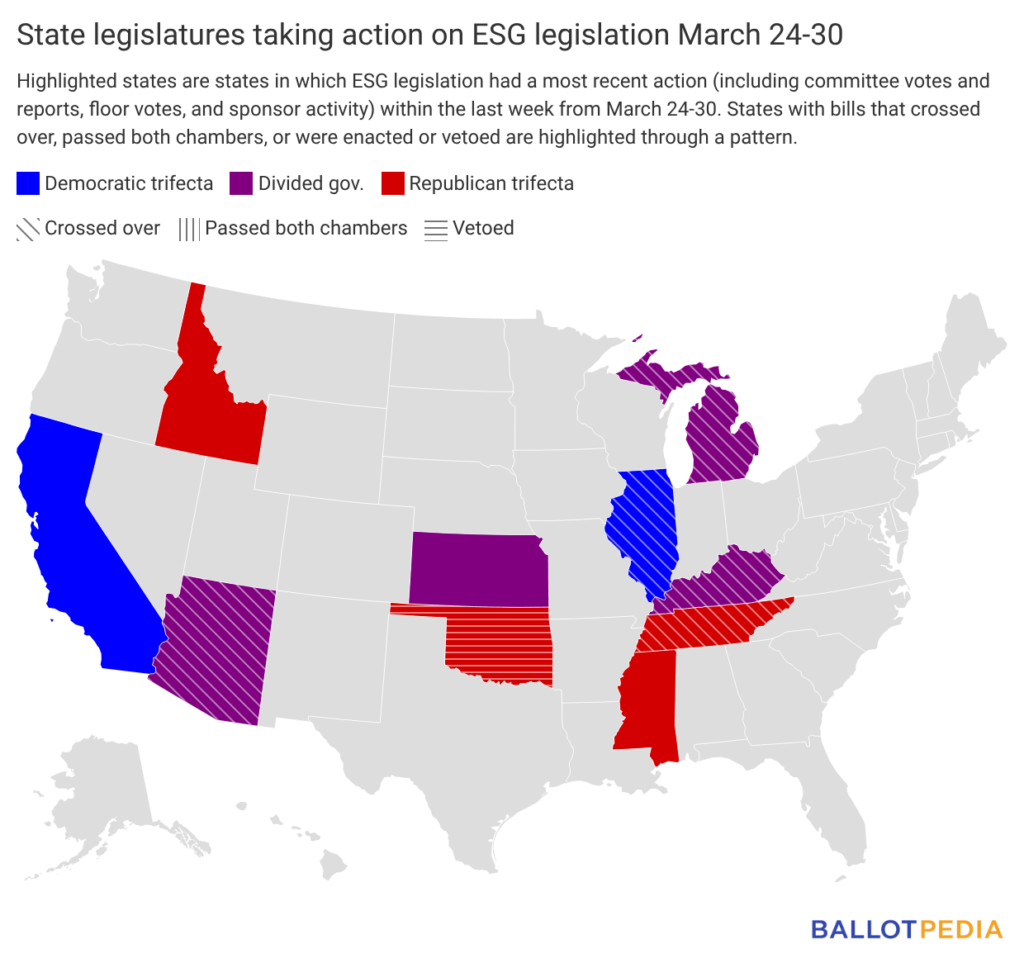

ESG legislation update

Ten states took action on 23 ESG-related bills last week (since March 24).

States with legislative activity on ESG last week are highlighted in the map below. Click here to see the details of each bill in the legislation tracker.

On Wall Street and in the private sector

BlackRock CEO doesn't mention ESG in annual letter

What’s the story?

Larry Fink, CEO of BlackRock, published his annual letter to investors on March 23, 2026, warning that Social Security may not pay full benefits by 2033 and endorsing a bipartisan Social Security reform proposal from Sens. Bill Cassidy (R-La.) and Tim Kaine (D-Va.). The proposal would create a $1.5 trillion investment fund, financed through federal borrowing and invested in stocks and bonds, to supplement Social Security over time.

Fink said inaction was a risk to promised benefits:

I understand why any talk of changing Social Security makes people uneasy. Social Security is a core promise, and people rightly believe it should be honored. But under the current system, doing nothing could very well break that promise. Current projections show the trust fund won't be able to pay full benefits by 2033. Many young Americans doubt they'll ever fully see theirs. Addressing that gap will likely require multiple solutions. But thoughtful, long-term investing could be one of them.

Why does it matter?

Fink signals continued focus on retirement policy and a shift away from environmental, social, and governance (ESG) investing at one of the world’s largest asset managers. His support for the Cassidy-Kaine proposal places BlackRock in the ongoing policy debate over how to address Social Security’s long-term funding gap, as some projections indicate the program may not be able to pay full benefits in the early 2030s without changes.

Fink also emphasizes expanding access to long-term investing as a way to build wealth, arguing that more Americans currently lack the savings needed to participate in financial markets. Fink points to policies such as emergency savings accounts and early investment programs as ways to increase participation, framing retirement security as tied to broader access to capital markets.

Companies split on ESG proposal lawsuits

What’s the story?

Companies have taken different approaches to investor lawsuits over proxy proposals, with some agreeing to include proposals after being sued and others contesting the claims in court. Investors have filed at least six lawsuits since March 2026 seeking to force companies to include proposals on proxy ballots, following a policy shift at the Securities and Exchange Commission (SEC).

The agency said in November 2025 it would no longer issue most no-action letters — staff guidance that previously indicated whether companies could exclude shareholder proposals from proxy ballots. Since then, investors have filed at least six lawsuits, including a March 20 case against UnitedHealth Group Inc., challenging companies’ decisions to block proposals.

Companies have taken different approaches:

- PepsiCo Inc. and AT&T Inc. quickly settled lawsuits and agreed to include proposals

- Axon Enterprise Inc. also reached a rapid settlement after initially contesting a case

- Chubb Ltd. and BJ’s Wholesale Club Holdings Inc. have chosen to fight the lawsuits in court

Some companies say the lawsuits are unnecessary, while investor groups say litigation now serves as the primary way to enforce shareholder rights.

What’s the background?

Two investor groups — the Interfaith Center on Corporate Responsibility and As You Sow — filed a lawsuit on March 19, 2026, in U.S. District Court for the District of Columbia challenging the SEC’s decision to stop issuing most no-action letters. The groups said the agency changed how it applies Securities Exchange Act Rule 14a-8, which governs shareholder proposals, without following the Administrative Procedure Act’s rulemaking requirements.

Rule 14a-8 allows shareholders to submit proposals for inclusion in company proxy statements and permits companies to seek SEC staff guidance on whether they can exclude those proposals. The SEC has historically provided that guidance through no-action letters indicating whether staff would recommend enforcement if a company omits a proposal.

In November 2025, the SEC’s Division of Corporation Finance said it will not respond to most no-action requests for the 2025–26 proxy season, citing time and resource constraints following a 42-day federal government shutdown. Chairman Paul Atkins said the agency would use the proxy season to evaluate whether to resume reviewing these requests.

ESG funds shrink despite rising asset values

What’s the story?

U.S. ESG funds contracted in 2025, with investors withdrawing $21 billion and fund closures far exceeding new launches, extending a three-year decline in the sector, according to Morningstar data.

Total ESG fund assets reached roughly $368 billion at the end of 2025, mostly due to market gains rather than new investment.The number of ESG funds declined, with 91 funds closing and only nine launching, resulting in a net loss of 82 funds.

Why does it matter?

The figures show investor demand for ESG funds remains weaker than for the broader fund market, where inflows continued in 2025. Continued outflows and fund closures suggest firms are scaling back ESG offerings or consolidating products as interest declines.

At the same time, rising asset values indicate ESG funds remain widely held and tied to broader market performance. That dynamic—declining inflows alongside growing total assets—suggests the sector’s size depends more on market conditions than on new investor demand.