Economy and Society is Ballotpedia’s weekly review of the developments in corporate activism; corporate political engagement; and the Environmental, Social, and Corporate Governance (ESG) trends and events that characterize the growing intersection between business and politics.

ESG Developments This Week

Election preview

Across the country, voters are gearing up to decide the control of the U.S. Senate, U.S. House, and state governments nationwide. Beyond the usual high-profile races, let’s take a look at another set of important offices: state financial officers (SFOs).

Different states have different names for these elected officials, but they all fall into three groups: treasurers, auditors, and controllers. Broadly, these officials are responsible for things like investing state funds, auditing other government offices, and overseeing pensions.

When it comes to where the money goes and who is watching it, these officeholders are typically the ones in charge, giving them an important role in state government. Like gubernatorial elections, the midterm election cycle is disproportionately weighted with a majority of the elections in four-year cycles.

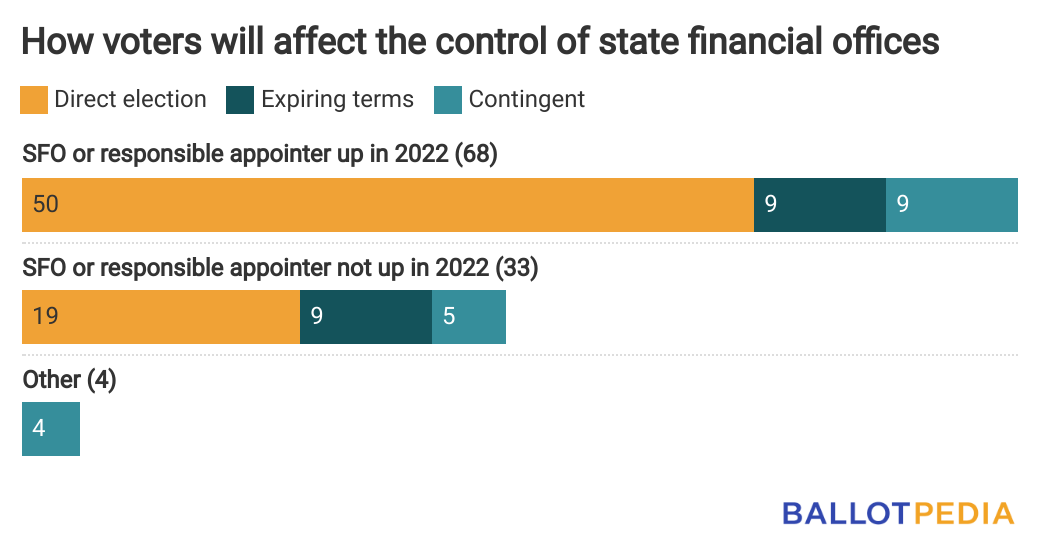

In 2022, either directly or indirectly, voters will decide who controls 68 of the 105 state financial officerships nationwide (65%).

- Direct elections: voters will directly elect 50 SFOs this year. For comparison, only 14 are on the ballot in 2024.

- Appointees with expiring terms: nine SFOs’ terms are set to expire in 2023 or 2024, with decision-making power for the next term falling to the governors and legislators voters elect this November.

- Contingent appointees: nine SFOs’ don’t have a term length, but instead serve at the pleasure of elected officials who are on the ballot this year. If an elected official loses or the office switches party control, their predecessor will get to decide whether to keep those SFOs or appoint new ones.

- Other: four SFOs’ terms are contingent upon either a non-elected appointee or a multi-member board.

Among the 36 appointed SFOs, 28 are appointed by a single office or entity:

- Governors appoint nine

- Legislatures or joint legislative committees appoint 14;

- In Oregon, the secretary of state appoints the auditor; and,

- Other appointees or multi-member boards appoint four.

Additionally, offices sometimes have to work together to select SFOs:

- Governors appoint, and legislatures confirm, two SFOs;

- Governors appoint, and senates confirm, five; and,

- In Wyoming, the governor, secretary of state, and treasurer, by majority vote, appoint the auditor, with the Senate’s confirmation.

When it comes to partisan affiliations, most appointed SFOs are officially nonpartisan, but we can use the party of the appointing authority to make an estimation. But this is not always a perfect calculation, as it is not uncommon for an appointer of one party to retain an SFO appointed by a member of a different party.

In Oregon, for example, former Secretary of State Dennis Richardson (R) appointed Kip Memmott as the state’s audit director in 2017. Memmott remained in office even after Secretary of State Shemia Fagan (D) took control in 2021.

And in Virginia, Controller David Von Moll took office in 2001, under former Gov. Jim Gilmore (R). Von Moll then remained controller throughout four Democratic administrations over the following two decades.

The 69 directly-elected officers, on the other hand, hold partisan positions, meaning candidates run with party labels on the ballot.

Altogether, heading into November, there are

- 42 SFOs who are Democrats or were appointed by Democrats;

- 56 SFOs who are Republicans or were appointed by Republicans;

- Three SFOs who were appointed by a combination of Democrats and Republicans, listed as other; and,

- Four SFOs who were appointed by non-elected appointees or multi-member boards, also listed as other.

Among the offices being decided this November, Democrats and Republicans both currently hold 33, and two positions are marked as other because appointment authority was split between Democrats and Republicans.

In Washington, D.C., and around the world

UK announces stricter rules for businesses’ ESG claims

The British financial regulator, the Financial Conduct Authority (FCA), announced last week that it would follow the lead of regulatory bodies in other Western nations (including the American Securities and Exchange Commission) in developing regulations related to preventing and punishing false or misleading ESG claims from businesses:

“The UK’s financial regulator made clear it will no longer tolerate vague ESG fund designations as it moves to crack down on investment managers that can’t back up their claims of targeting environmental, social and governance metrics.

Fund managers operating in the UK will face a “package of new measures, including investment product sustainability labels and restrictions on how terms like ‘ESG,’ ‘green’ or ‘sustainable’ can be used,” the Financial Conduct Authority said in a statement on Tuesday.

It’s the latest example of regulators tightening the screws around ESG investing, which after years of unfettered growth now accounts for roughly a third of global assets. A more aggressive regulatory environment has already led asset managers to scale back their ESG ambitions, with an analysis by Jefferies showing that reclassifications to package regular funds as more sustainable products plunged 84% over the past year.

“Already today, greenwashing may be eroding trust in the market for sustainable investment products,” the FCA said. “If consumers can’t trust the claims firms make about their products, they will shy away from this market, slowing the flow of much-needed capital to investments that can genuinely drive positive change.”

The watchdog expects the bulk of the proposed rules will come into effect in mid-2024 at the earliest.

Regulators in the EU, US, UK and Japan are stepping up oversight of ESG funds amid growing concerns that asset managers keen to sell products are promising more than they can deliver. Fund clients have been calling for better guardrails on the ESG industry, with an analysis by PwC showing that 71% of institutional investors want stronger ESG regulations. The hope is that extra rules “can act as an important lever to build trust and decrease the risk of mislabeling,” according to PwC….

The FCA proposed three fund labels: “Sustainable Focus,” which invests mainly in assets that achieve a high standard of sustainability; “Sustainable Improvers,” which would invest in assets that may not be sustainable now with an aim to improve them; and “Sustainable Impact,” which targets solutions to social and environmental challenges.”

UK’s Advertising Standards Authority orders a stop on ESG advertising from HSBC

The UK’s Advertising Standards Authority (ASA) ordered HSBC – the largest bank in Europe – to stop a poster advertising campaign that depicted the bank as environmentally friendly. The regulator said the posters violated environmental advertising rules because they omitted information about the bank's investments in businesses and industries that generated high levels of carbon emissions:

“HSBC Holdings Plc has been reprimanded by a UK watchdog for violating environmental advertising rules, after it sought to depict itself as a green bank in a set of posters.

In the latest sign that regulators are growing increasingly intolerant of all manifestations of greenwashing, the Advertising Standards Authority said it has ordered HSBC to ensure the posters “not appear again in the form complained of,” according to a statement published Wednesday.

HSBC breached the so-called CAP Code, which relates to non-broadcast advertising and direct and promotional marketing, the ASA said. The bank was told to make sure that “future marketing communications featuring environmental claims were adequately qualified and didn’t omit material information about its contribution to carbon dioxide and greenhouse-gas emissions,” the watchdog said….

HSBC’s advertisements drew complaints from environmental groups, which said they misled consumers. The two posters in question, which were used by HSBC ahead of last year’s COP26 climate summit, stated that the bank plans to “provide up to $1 trillion in financing and investment globally to help our clients transition to net zero,” and that it’s “helping to plant two million trees, which will lock in 1.25 million tons of carbon over their lifetime.”…

HSBC has helped arrange about $111 billion of financing for fossil-fuel companies since the Paris climate accord was struck in late 2015. More than half of that was in the form of loans to oil, gas and coal clients, according to data compiled by Bloomberg.

The ASA said that, “despite the initiatives highlighted in the ads,” HSBC was “continuing to significantly finance investments in businesses and industries that emitted notable levels of carbon dioxide and other greenhouse gasses,” which consumers might not realize based on the information in the posters.

“We concluded that the ads omitted material information and were therefore misleading,” the ASA said.”

In Washington, D.C.

Chairman of the Senate Intelligence Committee says ESG-favored companies often ignore environmental and social abuses in China

Two weeks ago, U.S. Senator Mark Warner (D), the chairman of the Senate Intelligence Committee, argued that some companies only talk about their ESG credentials in American and Western settings. In his book The Dictatorship of Woke Capital, market analyst Stephen Soukup argued that one of the primary problems with ESG-favored companies, in his view, was their disparate treatment of environmental and social issues in Western nations on the one hand and the People’s Republic of China on the other. Warner said companies like Apple and Tesla often ignore environmental and social abuses in countries like China:

“Senate Intelligence Committee Chairman Mark Warner said he’s “disappointed” that companies such as Apple Inc. and Tesla Inc. tout their ESG bona fides but neglect glaring environmental or human rights issues when relying on China for supply chains and sales.

Multinationals may highlight their commitment to Environmental, Social and Governance goals but also reason that “the Chinese markets, it’s so big, we’ve got to turn a blind eye” to abuses, Warner said in an interview with Bloomberg in New York. “Whether it’s oppression of the people in Hong Kong or whether it’s the Uyghurs or whether it’s using electrical power coming out of Xinjiang to build the batteries that go in your Tesla.”

China has been accused of widespread human rights abuses against mostly Muslim Uyghurs in the far west region of Xinjiang,

Warner said he’s “disappointed with our friends at Apple” and has been “really frustrated with not just American companies, but other multinationals.”

Spokespeople for Apple and Tesla didn’t immediately return emails seeking comment on Tuesday. Sales in China accounted for roughly a quarter of Tesla’s automotive revenue in the third quarter. Apple are 99% made in China, according to Bloomberg Industries, and about a fifth of its revenue comes from China….

Warner predicted additional legislative action on the issue, including on synthetic biology, advanced energy, quantum computing and other emerging technologies.

Warner also critiqued some environmentalists for measuring the impact of electric cars based only on when the vehicle is used as opposed to “how the car got got to your driveway in the first place.””

On Wall Street and in the private sector

73% of large American companies consider ESG data in determining executive compensation according to a new report

A new report out this week says that 73% of all large American companies consider ESG metrics to varying degrees in determining executive compensation levels:

“Large US companies are increasingly linking executive compensation to some form of ESG performance, with the share growing from 66 percent in 2020 to 73 percent in 2021. At the same time, just a minority of polled corporate executives say including ESG (environmental, social, and governance) performance goals in executive pay is very important in achieving their ESG goals. Most view such measures as being of medium importance, which indicates that incorporating ESG measures into compensation is just part of companies' broader efforts to achieve their objectives.

The findings come from a new report by The Conference Board, produced in collaboration with Semler Brossy and ESG data analytics firm ESGAUGE. The study includes various trends—and highlights lessons learned—relating to companies tying executive pay to ESG performance.

In addition to the analysis showing an overall increase in the adoption of such goals, some ESG topics have gained considerably more traction than others: From 2020 to 2021, the share of S&P 500 companies incorporating DE&I (diversity, equity and inclusion) goals in executive compensation grew from 35 percent to 51 percent. And carbon footprint and emission goals nearly doubled, increasing from 10 percent to 19 percent.

To understand the opportunities and challenges companies have in implementing ESG performance goals in executive compensation programs, The Conference Board convened a roundtable with executives in compensation, ESG, governance, and sustainability. Participants said the top reason to link executive pay to ESG performance goals is signaling ESG as a priority, followed by responding to investor expectations. The top two reasons for not tying executive compensation to ESG is the challenge of defining specific goals, followed by skepticism about their effectiveness.”

In the spotlight

Finnish study suggests net zero carbon emissions might be impossible due to limited battery resources

A new Finnish government study says the limited availability of natural resources such as cobalt could limit battery production at the scale needed to reach net zero carbon emissions globally. According to the Daily Skeptic:

“Influential elites are either in denial about the horrifying costs and consequences of Net Zero – witness last Wednesday’s substantial vote against fracking British gas in the House of Commons – or busy scooping up the almost unlimited amounts of money currently on offer for promoting pseudoscience climate scares and investing in impracticable green technologies. Until the lights start to go out and heating fails, they are unlikely to pay much attention to a recent 1,000 page alternative energy investigation undertaken for a Finnish Government agency by Associate Professor Simon Michaux. Referring to the U.K.’s 2050 Net Zero target, Michaux states there is “simply not enough time, nor resources to do this by the current target”.

To cite just one example of how un-costed Net Zero is, Michaux notes that “in theory” there are enough global reserves of nickel and lithium if they are exclusively used to produce batteries for electric vehicles. But there is not enough cobalt, and more will need to be discovered. It gets much worse. All the new batteries have a useful working life of only 8-10 years, so replacements will need to be regularly produced. “This is unlikely to be practical, which suggests the whole EV battery solution may need to be re-thought and a new solution is developed that is not so mineral intensive,” he says.

All of these problems occur in finding a mass of lithium for ion batteries weighting 286.6 million tonnes. But a “power buffer” of another 2.5 billion tonnes of batteries is also required to provide a four-week back-up for intermittent wind and solar electricity power. Of course, this is simply not available from global mineral reserves, but, states Michaux, it is not clear how the buffer could be delivered with an alternative system.

Michaux sounds a clear warning message. Current expectations are that global industrial businesses will replace a complex industrial energy ecosystem that took more than a century to build. It was built with the support of the highest calorifically dense source of energy the world has ever known (oil), in cheap abundant quantities, with easily available credit and seemingly unlimited mineral resources. The replacement, he notes, needs to be done when there is comparatively very expensive energy, a fragile finance system saturated in debt and not enough minerals. Most challenging of all, it has to be done within a few decades. Based on his copious calculations, the author is of the opinion that it will not go fully “as planned”.”