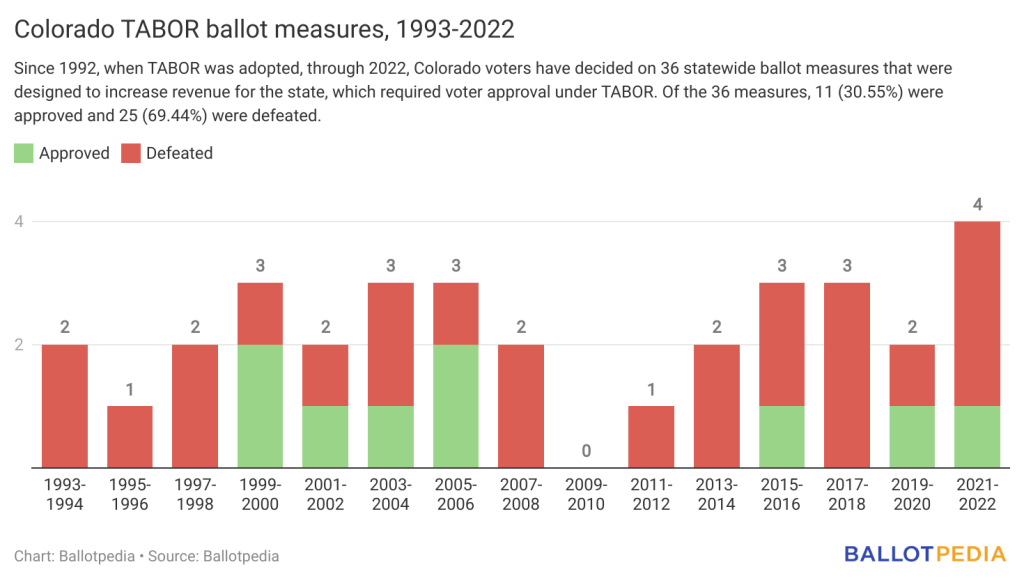

Coloradans have decided on 36 statewide ballot measures that were designed to increase revenue for the state, which required voter approval under TABOR. Of the 36 measures, 11 (30.56%) were approved and 25 (69.44%) were defeated.

Colorado's Taxpayer's Bill of Rights (TABOR), adopted in 1992, was designed to require statewide voter approval of all new taxes, tax rate increases, extensions of expiring taxes, mill levy increases, valuation for property assessment increases, or tax policy changes resulting in increased tax revenue.

Of the 36 measures, 17 were referred to the ballot by the state legislature and 19 were placed on the ballot through citizen initiative petitions. Of the 11 approved measures, 10 were referred to the ballot by the state legislature and one was a citizen initiative.

Highlights:

- 14 of the measures were designed to increase a tax. Of the 14 measures, two were approved and 12 were defeated. In 2004, voters approved an initiative to increase the tobacco tax to fund educational and healthcare programs. In 2020, voters approved a measure placed on the ballot by the state legislature to increase tobacco taxes and create a tax on nicotine products to fund health and education programs.

- 10 of the 36 measures asked voters if the state could retain and spend revenue over the TABOR limit as a voter-approved revenue change. Of the 10 measures, three were approved and seven were defeated. One of the approved measures, Referendum C, created a new cap on state revenue, called the Referendum C cap. Referendum C authorized the state to retain and spend all of the money it collected above the TABOR limit on healthcare, public education, transportation projects, and local fire and police pensions for five years beginning with fiscal year (FY) 2005-06. During these five years, Colorado residents did not receive the refunds they would have otherwise received under TABOR. After the five-year period, referred to as the timeout period, Referendum C authorized the state to permanently retain and spend revenue up to a cap, referred to as the Referendum C cap (equaling FY 2007-08 revenues adjusted by inflation plus population growth), beginning in FY 2010-11.

- Five of the measures proposed creating a new tax. Two were approved and three were defeated. In 2013, voters approved a measure referred by the state legislature that established taxes on marijuana sales. In 2019, voters approved a measure referred by the state legislature that legalized sports betting and created a tax on sports betting proceeds to fund state water projects.

- Five of the measures proposed issuing bonds and increasing state debt, using proceeds from the bonds to fund various projects. Two bond issue measures were approved and three were defeated.

- Two other measures, which were both approved, increased state revenue in other ways. In 2006, voters approved a legislatively referred measure that eliminated a state income tax credit for businesses that employed undocumented immigrants. Most recently, in 2022, voters approved Proposition FF, a legislatively referred measure that reduced income tax deduction amounts to fund a school meals program.

In 2023, Colorado voters will decide on two measures referred to the ballot by the state legislature that require voter approval under TABOR.

One measure, Proposition HH, would reduce property tax rates and allow the state to retain and spend revenues that would otherwise be refunded to residents under TABOR. Proposition HH would allocate this revenue to local governments for the purpose of making up lost tax revenues from the property tax rate reduction. The measure would make other changes to property tax law and create a Proposition HH Cap on state revenue, similar to the Proposition C cap, which authorized the state to permanently retain and spend revenue up to a cap, referred to as the Referendum C cap (equaling FY 2007-08 revenues adjusted by inflation plus population growth), beginning in FY 2010-11.

The other measure, Proposition II, asks voters whether the state can keep and utilize excess revenue ($23.65 million) generated from increased and new tobacco, cigarette, and nicotine taxes approved by voters in 2020 through Proposition EE, or whether the excess revenue will be refunded to distributors and wholesalers and tax rates set by Proposition EE will be reduced. If the ballot measure is approved, the state would be permitted to keep and use revenue that exceeded the estimated amount generated from those taxes. This additional revenue, which amounts to $23.65 million, would be allocated to the state's universal preschool program, which is the current primary recipient of Proposition EE funds. The tax rates established in Proposition EE would remain unchanged. If the ballot measure is rejected, the state would be required to refund the $23.65 million in excess revenue to tobacco and nicotine product distributors and wholesalers. If the measure is rejected, the tax rates on tobacco, cigarettes, and nicotine products under Proposition EE would be reduced by a total of 11.53%.

Additional reading: