In this week’s edition of Economy and Society:

- European Commission to drop greenwashing rule

- ESG legislation update

- American banks increased fossil fuel investments in 2024

- Bernstein report suggests ESD rather than ESG considerations

- Microsoft invests in carbon capture

- Stuttaford argues ESG has always been political

Around the world

European Commission to drop greenwashing rule

What’s the story?

The European Commission (EC) announced plans June 20 to withdraw its Green Claims Directive, a proposed regulation that would have required companies to substantiate environmental marketing claims—such as carbon neutral or eco-friendly—that lacked clear standards.

Why does it matter?

The withdrawal is part of a broader shift in the EC’s approach to environmental regulation. After introducing several ESG-related proposals in recent years, the Commission has reevaluated and scaled back measures. Some European officials have cited business competitiveness concerns—especially amid reduced ESG momentum in the United States—as a reason for the change.

What’s the background?

For more on the EU’s move away from ESG, click here.

Read more

According to ESG Today:

The European Commission revealed on Friday that it plans to withdraw the Green Claims Directive just days prior to trilogue negotiations to finalize the proposed rules aimed at protecting consumers from greenwashing claims about the environmental attributes of products and services, following objections from lawmakers that brought its ability to be adopted into doubt. …

The withdrawal follows two years of negotiations in the EU Parliament and Council over the proposal. The Commission introduced the directive in March 2023, aimed at addressing a need for reliable and verifiable information for consumers, in light studies finding that more than half of green claims by companies in the EU were vague or misleading, and 40% were completely unsubstantiated.

The Commission’s proposal included minimum requirements for businesses to substantiate, communicate and verify their green claims, obligating companies to ensure the reliability of their voluntary environmental claims with independent verification and proven with scientific evidence. The directive also targeted the proliferation of private environmental labels, requiring them to be reliable, transparent, independently verified and regularly reviewed, and allowing new labels only if developed at the EU level, and approved only if they demonstrate greater environmental ambition than existing label schemes.

In the states

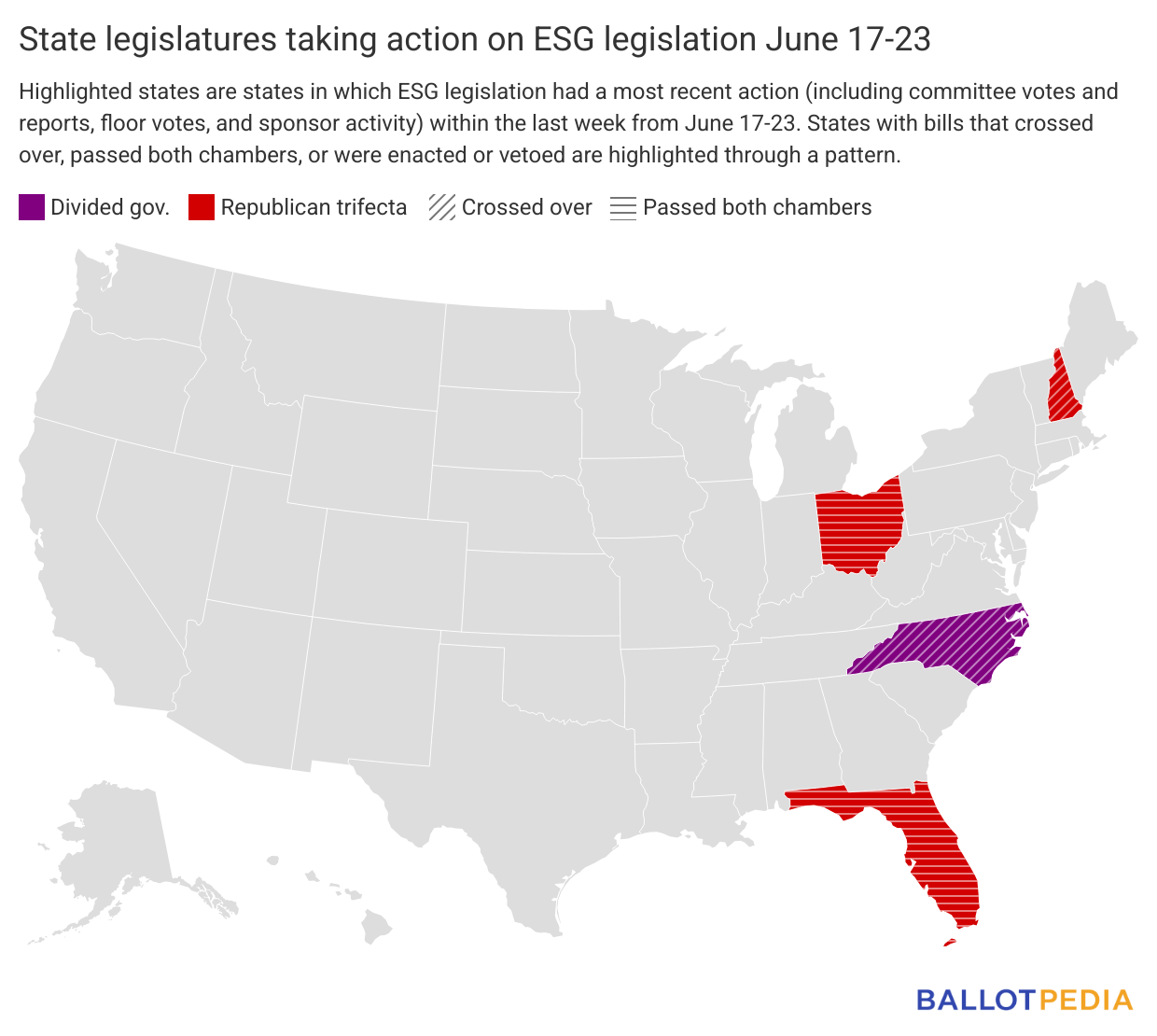

ESG legislation update

Four state legislatures took action on six ESG-related bills last week (since June 17). Legislation in Ohio and Florida passed both chambers. Legislation in New Hampshire and North Carolina crossed over from one chamber to another.

States with legislative activity on ESG last week are highlighted in the map below. Click here to see the details of each bill in the legislation tracker.

On Wall Street and in the private sector

American banks increased fossil fuel investments in 2024

What’s the story?

A new report from several climate organizations—including Rainforest Action Network, Sierra Club, and Reclaim Finance—found that the four largest U.S. banks increased their fossil fuel financing $162.5 billion in 2024.

Why does it matter?

The report found that 45 of the world’s largest banks increased fossil fuel financing in 2024, with the four largest U.S. banks accounting for roughly 21% of the total. The groups said the increase reversed prior years of declining investments.

The findings align with recent bank departures from climate alliances and adjustments to environmental commitments.

Read more

According to ESG Dive:

The report from the Rainforest Alliance Network, Sierra Club, Reclaim Finance and other climate organizations found that the 65 largest global banks committed $869 billion to fossil fuel companies in 2024, as 45 of the covered banks increased their year-over-year fossil fuel financing. The top four U.S. banks — JPMorgan Chase, Bank of America, Citi and Wells Fargo — represented 21% of total global fossil fuel financing accounted for in the report.

RAN Senior Research Strategist Caleb Schwartz, one of the report’s co-authors, called it a “pretty significant year for the report given the reverse in trajectory.

“We’re seeing a pretty substantial increase between 2023 and 2024, and we track these annual increases as an indicator of the banks’ commitment,” Schwartz said in an interview with ESG Dive. “Banks are putting money into fossil fuels, they’re putting money into fossil fuel expansionism.”

Bernstein report suggests ESD rather than ESG considerations

What’s the story?

Analysts at Bernstein recommended in a recent report to clients that investors shift from focusing on ESG investment factors to what they called ESD—emerging, strategic, and disruptive considerations.

Why does it matter?

As some institutional investors move away from using the term ESG, analysts and firms are adjusting their frameworks to incorporate similar considerations under different labels. Bernstein described its ESD approach as a way to integrate environmental and social issues into broader assessments of long-term strategic risk.

Read more

According to The Financial Times:

According to analysts at Bernstein, investors need to pay more attention to “ESD” — emerging, strategic and disruptive factors. In a recent paper for clients, they argued that investors should take a more expansive view of the issues that affect how companies are positioned for “a future that is being reshaped in real time”.

These would include environmental and social risks and impacts, as well as vulnerabilities to geopolitical upheaval and the disruption caused by artificial intelligence advances.

Top ESD issues for the automotive sector, for example, would include regulations around carbon emissions, access to critical minerals, protectionist trade policies, and worker “talent gaps” linked to the long-term shift to electric and autonomous vehicles.

Microsoft invests in carbon capture

What’s the story?

Microsoft announced a series of carbon capture investments as part of its effort to meet its goal of becoming carbon-negative by 2030.

Why does it matter?

Microsoft’s latest sustainability report shows the company’s overall emissions have increased nearly a quarter since 2020, driven in part by expanding data center operations. The company’s carbon removal investments are one way it’s trying to maintain its climate pledges. Increased energy demand from artificial intelligence is complicating corporate emissions reduction goals.

Read more

According to Bloomberg:

Five years ago, Microsoft Corp. set a goal of becoming carbon negative by 2030 and removing all its historic emissions from the atmosphere by 2050. But the company’s artificial intelligence investments have made meeting those targets harder—by a lot. Today, Microsoft’s total planet-warming impact is 23% higher than it was in 2020 in part because of its vast expansion of emissions-intensive data centers, according to its 2025 sustainability report. …

Microsoft made a string of record carbon removal purchases this year, including a 3.7 million-metric-ton deal with CO280, a startup that captures CO₂ from pulp and paper mills, and a 6.8 million-metric-ton deal with AtmosClear, which is developing a carbon capture facility in Louisiana.

In the spotlight

Stuttaford argues ESG has always been political

What’s the story?

National Review editor Andrew Stuttaford argued in a June 20 piece that ESG is inherently political, building on Robert Verbruggen’s review from earlier this month of a study arguing ESG politicized corporate speech.

Why it matters:

One topic of the ESG debate centers on whether it functions as a neutral risk-management tool or as a means for advancing political or social goals. Stuttaford argues that both the study and Verbruggen’s review support the view that ESG is political in both origin and application.

What’s the background?

For more on Verbruggen’s article and the original study, click here.

Read more:

According to National Review’s Andrew Stuttaford:

In reality, ESG was, from its very beginnings as an idea promoted by the U.N. (a possible clue, I think, Dr. Watson), designed to advance a progressive agenda by diverting asset managers (and by extension corporate managements) away from what, barring specific instructions to the contrary, was their primary duty, generating investor and shareholder return. As such, it was a clever way of using other people’s money to promote changes better decided in a legislature than in the C-suite or on Wall Street. And as such it was not only a form of theft, but profoundly undemocratic.

This didn’t seem to worry the left, who were ESG’s beneficiaries, but eventually — and belatedly — the right caught on and started to push back, forcing a debate that Team ESG had wanted to avoid. Up to then, they had gotten away with it. Superficially ESG seemed rather technical, and thus (spot the faulty reasoning) unimportant. Moreover, it was in line with the growth of “stakeholder capitalism,” the idea that the shareholders who owned a business were just another group of “stakeholders” in the way a company was run. It was an idea fueled by an unappealing mixture of cowardice, greed, vanity, and self-promotion….

What eventually triggered the pushback by the right was the growth of increasingly assertive “woke capital,” which coincided with, in 2019, a notorious redefinition by the Business Roundtable of “corporate purpose” away from shareholder primacy to a stakeholder model. Anger over corporate wokery was both real and justified (and it was a more resonant rallying cry than a call for the defense of shareholder primacy). But the use of the w-word allowed ESG’s defenders to complain that their opponents were opening up another front in the “culture wars” (as if the creation of ESG and DEI were not) which, we are supposed to believe, are only fought by Republicans or the “far right.” In reality, at its core, the campaign against ESG was rooted in the defense of property rights and democratic principle.