ESG developments this week

Economy and Society is Ballotpedia’s weekly review of the developments in corporate activism; corporate political engagement; and the environmental, social, and corporate governance (ESG) trends and events that characterize the growing intersection between business and politics.

At Ballotpedia

States have passed 100 ESG bills since 2020

States have enacted 100 bills opposing and supporting ESG investing since 2020.

Overall, most Republican trifectas and states with divided governments have tended to support legislation opposing ESG. Most Democratic trifectas have tended to make laws supporting ESG investing. 92% of all bills passed on ESG since 2020 have come from:

- Republican trifectas opposing ESG (55 bills),

- Democratic trifectas supporting ESG (24 bills),

- Divided government states with Republican-controlled legislatures and Democratic governors opposing ESG (13 bills).

Today, we're going to take a deeper look at the specific policy approaches enacted in Republican and Democratic trifectas and examine which states have been the most and least active in supporting or opposing ESG.

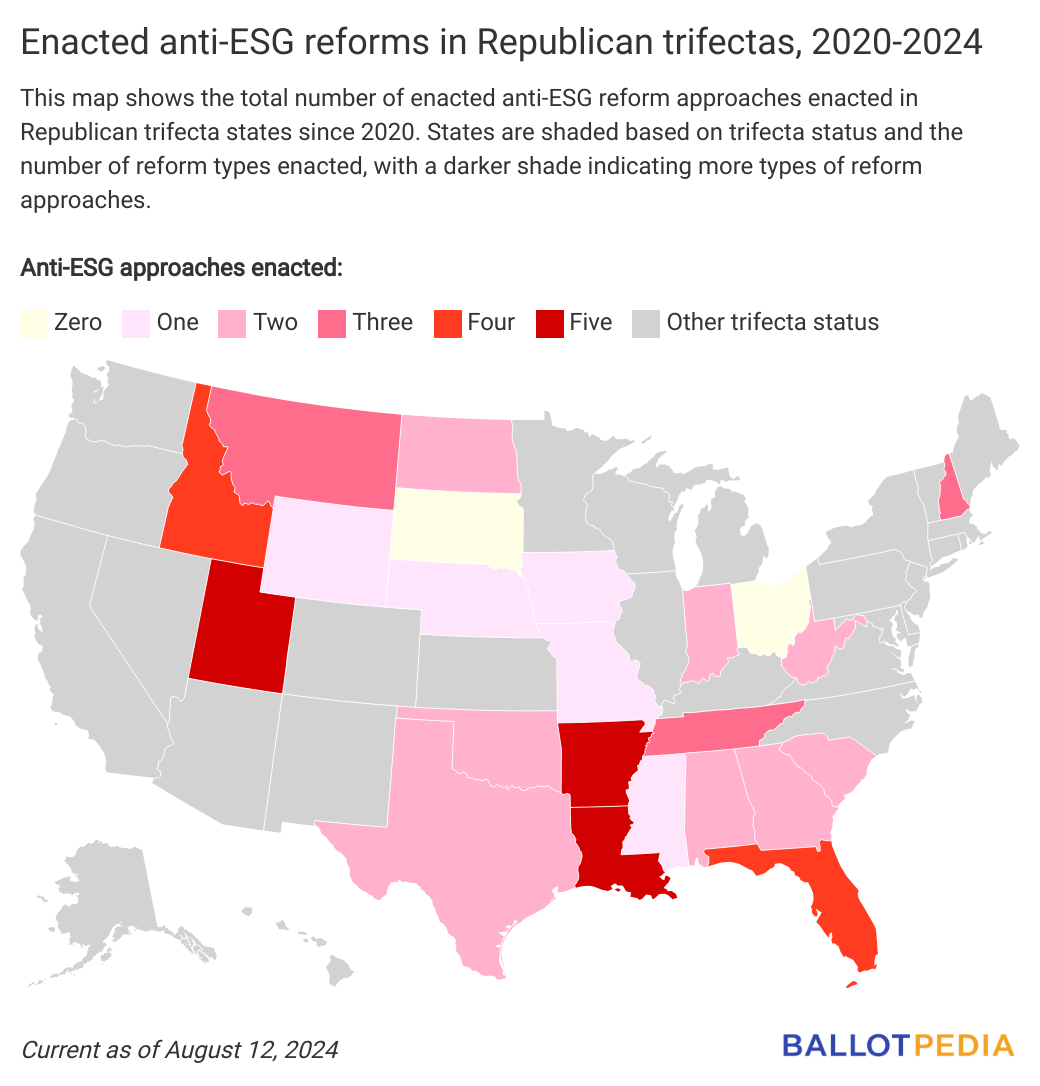

Republican trifectas opposing ESG

Twenty-three states currently have Republican trifectas, and 21 have made laws opposing ESG in five categories. Of those 21 states:

- 14 have enacted sole fiduciary legislation prohibiting or discouraging the consideration of ESG factors in public investments (like pension funds).

- 13 have enacted anti-boycott legislation prohibiting public contracts with or investments in companies that intentionally boycott certain companies or industries without a business purpose.

- 12 have enacted anti-discrimination legislation prohibiting banks and government agencies from using ESG scores (also known as social credit scores) to determine eligibility for financial services.

- 8 have enacted public disclosure requirement legislation requiring additional transparency surrounding the ESG policies, investments, and considerations of state investment boards and other government agencies.

- 6 have enacted legislation opposing federal ESG mandates that promote ESG investment standards.

The map below shows which Republican trifecta states have made the most laws opposing ESG since 2020:

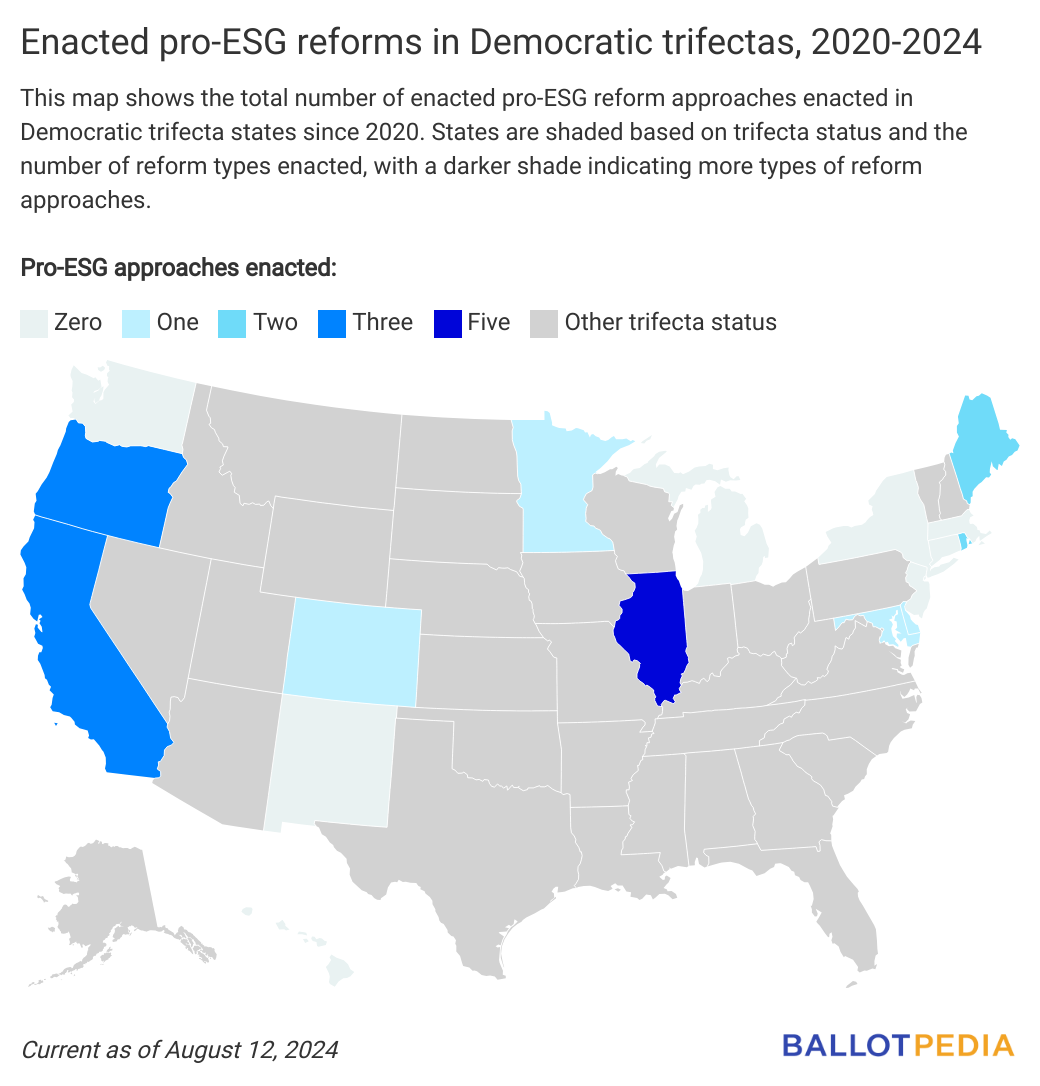

Democratic trifectas supporting ESG

Seventeen states have Democratic trifectas, and nine have made laws supporting ESG in five categories. Of those states:

- 5 enacted non-financial criteria consideration legislation requiring or allowing public fund managers to consider ESG data and other non-financial criteria in their investment strategies.

- 4 enacted industry divestment legislation prohibiting public investments in companies or industries that the government or agency considers environmentally or socially harmful.

- 4 enacted legislation requiring ESG criteria in state contracts.

- 3 enacted corporate board diversity legislation requiring publicly held companies to appoint a certain number of women, people of color, or people from other underrepresented groups to corporate boards of directors.

- 3 enacted corporate disclosure legislation requiring corporations to disclose certain types of ESG data, such as net emissions from business operations and climate-related risk factors.

The map below shows which Democratic trifecta states have made laws supporting ESG since 2020:

For more information and to stay abreast of enacted ESG developments by trifecta status, click here.

In Washington, D.C., and around the world

SEC files brief defending climate rule

The Securities and Exchange Commission submitted a brief to the U.S. Eighth Circuit Court of Appeals last week seeking to defend its rule requiring corporate climate disclosures. The agency argued environmental risks are relevant to investment decisions:

The U.S. Securities and Exchange Commission launched a defense in court of its new climate reporting rule, arguing that the proposed disclosures in the rule provide “information directly relevant to the value of investments,” and that it is within the Commission’s authority to mandate climate risk disclosures.

In a brief filed this week with the U.S. Eighth Circuit Court of Appeals, the Commission reiterated its view that “climate-related risks—and a public company’s response to those risks—can significantly affect a company’s financial performance and position,” yet current reporting on these risks are “inconsistent,” and “difficult to compare,” impeding the ability of investors to make decisions. …

In its filings, the Commission outlined its decision to adopt the new climate disclosure rule, highlighting a need for “more detailed, consistent, and comparable information,” and “substantial investor demand,” citing investor feedback, for climate-related information to help inform investment and voting decisions.

On Wall Street and in the private sector

Goldman Sachs Asset Management leaves climate group

Goldman Sachs Asset Management became the latest large U.S. fund manager last week to quit Climate Action 100+, an international organization that aims to coordinate ESG investments to reduce carbon emissions. U.S. lawmakers have recently investigated companies’ connections to the initiative:

U.S. members of global climate-focused coalitions have come under fire as some Republican lawmakers argue these groups might violate antitrust rules by encouraging companies to reduce climate-damaging emissions. This political tension was highlighted when a Republican congressional leader recently demanded over 130 investors to clarify their ESG goals.

A spokesperson for Goldman Sachs confirmed the exit, stating, “We’ve made investments in our ability to meet the sustainable investing needs of our clients and remain committed to leveraging our global capabilities.” This reflects the firm’s strategy to engage with companies independently, without the association with Climate Action 100+.

Goldman Sachs is not alone in this move. In the past few weeks, Aristotle Credit, Aristotle Pacific Capital, TCW Group, Vert Asset Management, Mellon Investment Corp, and Water Asset Management have also exited the group. Earlier this year, major players like Invesco, JPMorgan’s fund division, and State Street Global Advisors similarly withdrew.

ESG investment fund withdrawals continue

Withdrawals from ESG funds continued in the second quarter of 2024 according to data from Morningstar, meaning funds have shed more than they’ve taken in for nearly two years straight. But second-quarter losses were slower than in the first quarter. The largest funds continue to lose the greatest amounts:

Investors pulled $4.7 billion from US sustainable funds in the second quarter of 2024, making it the seventh-consecutive quarter of outflows. These outflows, however, were half of those experienced in the first quarter, which amounted to almost $9 billion. …

Although the motivations behind outflows cannot be precisely quantified, several key factors contribute to this trend. These include high interest rates, which have made alternative investment options more appealing and diminish the attractiveness of sustainable funds. Additionally, the mediocre returns of sustainable funds in 2023 have led to investor dissatisfaction and subsequent withdrawals. Concerns about greenwashing have also contributed to reduced investor confidence, as skepticism grows regarding the genuine sustainability credentials of some funds. Furthermore, the increasing politicization and regulatory scrutiny of ESG investing have prompted some investors to reevaluate their positions, resulting in further outflows. …

Topping the outflows table was Parnassus Core Equity Fund PRBLX, with redemptions of $758 million. Long known as the largest US sustainable fund, Parnassus Core Equity has been one of the 10 biggest losers in terms of redemptions for more than two years straight, shedding more than $5 billion over that period.

Governance considerations popular as environmental and social factors lose support

Shareholders were more supportive of governance proposals than environmental or social measures in annual meetings between January and June. ESG critics have argued that governance factors are distinct from the other two:

Shareholders asked to approve new ESG policies are warming up to the "G" even as they continue withholding support for the "E" and "S."

"G" refers to corporate “governance" changes, and such proposals received considerably more shareholder support this year than proposals targeting environmental (E) or social (S) changes, according to an analysis of ISS-Corporate data conducted by law firm Freshfields.

Of the 154 so-called governance proposals that went to a vote between Jan. 1 and June 14, 38 were successful, according to the analysis.