On Feb. 5, 2026, the Idaho Supreme Court unanimously upheld the state's private school choice refundable tax credit, rejecting the argument that the program violated the Idaho Constitution and judicial precedent.

The petitioners included the Committee to Protect and Preserve the Idaho Constitution, Inc., Mormon Women for Ethical Government, School District No. 281, Latah County, and the Idaho Education Association, Inc., among others. They filed a writ of prohibition with the Idaho Supreme Court in September 2025 to stop the program from proceeding, saying the program violated Article IX, section 1 of the Idaho Constitution and the public purpose doctrine.

Article IX, section 1 charges the Idaho Legislature with establishing and maintaining a "general, uniform, and thorough system of public, free common schools." The public purpose doctrine is a judicial precedent established by Idaho Water Res. Bd. v. Kramer in 1976, requiring government resources to primarily benefit public rather than private interests.

The opinion, written by Chief Justice G. Richard Bevan, held that Article IX, section 1, did not limit the legislature’s authority to do more than what the provision minimally required, and that the legislature has plenary authority to enact laws, so long as they are not unconstitutional.

Bevan held that the express intention of the tax credit was to increase education choice for parents. He said that since education was a public purpose, the tax credit did not violate the public purpose doctrine.

What is the Idaho Parental Choice Tax Credit?

On Feb. 27, 2025, Idaho Gov. Brad Little (R) signed House Bill 93 into law. It created the Idaho Parental Choice Tax Credit, which is a refundable tax credit for up to $5,000 per student enrolled in a private school, or $7,500 for students with qualifying disabilities. The legislature capped the program at $50 million annually; the bill required Idaho State Tax Commission to prioritize awarding refunds to families with an adjusted gross income below 300% of the federal poverty level. Though priority is given to families with income below a certain threshold, all families are eligible to apply.

Background

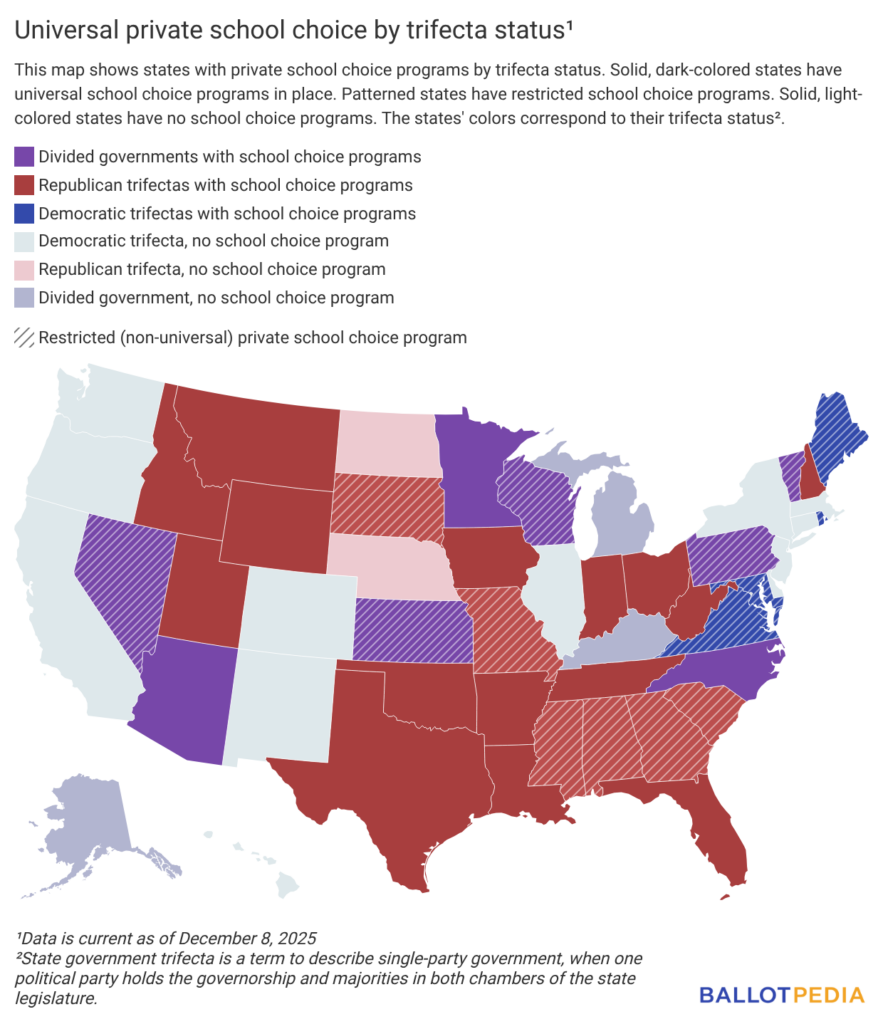

Ballotpedia defines private school choice programs as those that provide public funds for alternatives to public schools, such as private schools and homeschooling. A universal school choice program is one for which all students are eligible, regardless of family income, location, demographic, or disability. Non-universal school choice programs are available to a subset of qualifying students, such as students in families with income below a certain threshold, students with disabilities or special needs, or students zoned for certain schools or living in certain districts.

Eighteen (18) states run 24 universal private school choice programs. Of the 24 universal private school choice programs the states run, 10 are education savings account (ESA) programs, 10 are educational tax credit programs, and four are voucher programs. Some states run limited private school choice programs in addition to universal programs.

Education tax-credit programs provide tax incentives to individuals and businesses for supporting education and usually take one of the following forms:

- Tax-credit scholarships allow individuals and businesses to lower their tax burden by donating to scholarship funds, which provide private school tuition assistance.

- Individual tax credits/deductions allow families to reduce their state tax liability for approved education expenses, such as tuition, textbooks, or tutoring.

- Tax-credit ESAs allow tax credits for donations to fund Education Savings Accounts, which families can use for a range of educational expenses.

Depending on the tax credit program, the funds can be used for private or public educational expenses. As of Jan. 2026, 25 states had enacted tax-credit or tax-scholarship programs. Eleven states had implemented policies allowing individuals to write off or deduct educational expenses from their personal taxes.

Additional reading: